During one of the toughest years on record, the world’s central bankers were tested as never before.

Contributors: Gordon Platt, Antonio Guerrero, Anita Hawser and Dan Keeler

It is clear that 2009 is not a year on which the world’s central bankers will look back with undiluted pleasure. They can congratulate each other, however, on having survived this annus horribilis. Their actions may have assured that the world economy and financial system were saved—but at an enormous cost. Future generations will foot the bill for rescuing the financial world, unless the global economy recovers much more quickly and strongly than most economists expect. And those deserving central bankers who worked long hours to hold things together cannot afford to rest on their laurels. They must now consider the consequences of what they have done, or not done.

At some point it will become necessary to stop the presses from printing more money before another bubble forms. The Bank of Israel in August became the first major central bank to raise interest rates since the global economic crisis intensified in the wake of the fall of Lehman Brothers in September 2008.

Apart from making this tricky transition, central bankers need to be actively involved in the debate over how to avoid future crises involving systemic risk. To date, the financial system has not been noticeably reformed. The business of banking is slowly returning to usual. Incentives for performance remain focused on the short term. Financial engineers are designing new products, taking into account a slight toughening of regulations and a modest increase in capital requirements.

The financial system is in much better shape than it was a year ago, as central bankers around the world did whatever it took, or whatever they could, to limit the damage. Propping up financial institutions that are considered “too big to fail,” however, is not a sufficient remedy for restoring confidence. Much work remains to be done to ensure safe banking and economic prosperity.

The Americas

Argentina

Martin Redrado

Grade: C

While Martin Redrado continues to suffer from the Argentine administration’s lack of credibility on the financial front, particularly in underreporting inflation data, the central bank head has recently taken steps that could lead to Argentina’s return to the international financial community. Working with finance minister Amado Boudou, Redrado met with IMF Western Hemisphere chief Nicolás Eyzaguirre to discuss steps toward strengthening Argentina’s financial and monetary policies. President Cristina Fernández de Kirchner had sworn off the IMF during her presidential campaign, saying she hoped her grandchildren would not even know what the multilateral agency was. The Redrado-Boudou team traveled to London to attend the Group of 20 ministerial meetings to discuss joint strategies for tackling the global financial crisis. This is not to say Redrado has gone rogue, as the administration maintains a firm grip over central bank policy. But he has recently introduced initiatives that respond more to sound financial strategy than to political expediency. These include steps to promote local credit markets in order to create a peso yield curve and boost domestic liquidity. Unfortunately, his boss is not likely to loosen his reins anytime soon. In the financial chaos that is the current administration, analysts are giving Redrado credit for bringing some common sense to the table.

Brazil

Henrique de Campos Meirelles

Grade: B+

Henrique de Campos Meirelles’s prudent fiscal and monetary policies have helped Brazil navigate through the global economic downturn. After curbing inflation through a series of interest rate hikes, the central bank has since cut the benchmark Selic rate from 25% to July’s record-low 8.75%, contributing to the country’s economic recovery. Inflation fell from 17.2% in May 2003 to closer to 4% this year. Brazil is now expected to see year-on-year second-half 2009 GDP growth of as much as 8%, although analysts predict the economy could still shrink by 0.3% for full-year 2009. Meirelles is more optimistic and predicts a modest 0.8% expansion. Polls show consumer confidence growing steadily, so domestic demand should fuel more robust growth next year. Despite his high grades at the central bank, Meirelles, who served briefly in congress in 2002, may step down next April to enter the gubernatorial race for his home state of Goiás. President Luiz Inácio Lula da Silva, who publicly endorses Meirelles’s gubernatorial aspirations, would have to find a new central bank chief. Meirelles, Brazil’s longest-serving central bank president, would be a tough act to follow.

Canada

Canada

Mark Carney

Grade: B

No Canadian bank sought a government bailout or declared bankruptcy during the global financial crisis. The country’s conservative banking regulations helped create a climate in which Canada’s banks found it easier to obtain funding than banks in many other countries. As a result, the Bank of Canada found it necessary to extend less liquidity in relation to the size of Canada’s economy than did the United States and Britain. Mark Carney realized, however, that the strong Canadian dollar was offsetting the central bank’s stimulative monetary policy, and he allowed the overnight interest rate to remain at the effective lower boundary of 0.25% for an extended period. Firmer commodity prices and a rebound in business and consumer confidence are encouraging domestic demand growth at a time when inflation is under control. As a result, Canada is looking forward to economic growth of 3% or better for the next two years. Carney remains unpopular for his role in ending Canada’s income trusts—a tax loophole—when he was at the finance ministry, but he deserves credit for his sensible conduct of monetary policy.

Chile

Chile

José De Gregorio

Grade: B

While José De Gregorio’s term was off to a bumpy start on account of problems inherited from predecessor Vittorio Corbo, he has since shown his mettle by helping Chile remain among the region’s most stable economies. No Chilean bank has succumbed to the global financial crisis, as the country already had a strong regulatory framework and high banking standards. De Gregorio’s policies are contributing to restarting the nation’s economy by supporting the financial sector. The central bank’s actions have included suspending issuance of central bank bonds through year-end and extending 90- and 180-day loans to banks at preferential rates. While some countries are worried over soaring inflation and weakened currencies, De Gregorio is faced with the opposite, though no less worrisome, situation. The Chilean peso has strengthened 15% against the dollar this year, threatening exports and prompting De Gregorio to warn of possible central bank intervention in the foreign exchange market. On the price front, Chile now faces a deflation trend on falling consumer demand, with the 12-month inflation figure standing at a meager 0.3% in July, compared with a 3% full-year target. As former deputy central bank governor and member of the bank’s board of directors, De Gregorio brings an impressive resume that appears to be showing results in a challenging environment.

Mexico

Guillermo Ortiz

Grade: B

Mexico’s central banker is bringing a steady hand to an economy in crisis. With 80% of Mexican exports going to the United States, the US slowdown has hit the Mexican economy hard. Guillermo Ortiz has responded by rethinking fiscal and monetary policies. He has his work cut out. The government reported a $3.7 billion budget deficit in July on account of falling tax income, and the economy is expected to shrink by as much as 7% this year, presenting the greatest annual drop since 1932. However, Ortiz has stepped up to the plate, most importantly by taking a realistic stance and managing expectations for the government, investors and the general populace. The central bank halted interest rate cuts in August amid, albeit meager, signs of gradual economic recovery for next year. Ortiz predicts inflation will be 4% this year and 3% in 2010. The government has had some help from its friends, receiving $4 billion in IMF assistance to bolster reserves. This is in addition to the $47 billion IMF credit line received in April. Ortiz, convinced that the worst may be over, is now advocating for the government to reconsider its economic model in order to avoid its traditional international contagion.

United States

United States

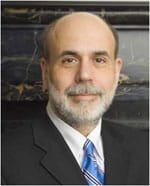

Ben Bernanke

Grade: C

Ben Bernanke is taking credit for saving the world from an economic disaster that he helped to create and failed to see coming. Bernanke and the US Treasury, with whom the Federal Reserve consorted, may have brought the economy and the financial system back from the brink, but they also must share the blame for planting the seeds of the next crisis. As a result of its massive debt, the United States is more at the mercy of foreign central banks than ever before. Foreign investors must be enticed to keep buying treasuries, or long-term US interest rates will shoot higher and dump the economy back in the drink. Financial markets and the economy seem to be in better shape than they were a year ago, and this may be due in large part to the raft of expensive stimulus programs floated by the Fed. It is impossible to know, however, what would have happened if Lehman Brothers had been saved, or if American International Group had been forced to sort out its own problems. The Fed and other central banks around the world pumped huge amounts of money into the markets to take care of short-term problems without regard to long-term consequences. It is true that the Fed responded quickly and aggressively to the worst crisis in generations. It remains to be seen, however, if it did the right thing. US president Barack Obama seems to think so. He reappointed Bernanke, a Republican, to a second term.

Europe

Hungary

Hungary

András Simor

Grade: B

Hungary’s central bank is very clear about its core mission: to achieve and maintain price stability. For a while this year the bank was on course to fulfill at least the first part of that mission, having hauled inflation down from nearly 9% to hit its target level of 3%. Maintaining it at that level has proved challenging, though, and the bank’s own forecasts suggest inflation will average out at 4.5% for 2009 and edge lower to 4.1% next year. While inflation is central bank governor András Simor’s primary focus, economic growth—or the lack of it—is proving even more troublesome. The bank has scrapped its earlier forecast of moderate economic growth for 2009 and now says GDP will shrink by a painful 6.7% and only begin to grow again some time next year. Even so, it is keeping interest rates moderately high with a promise to ease if inflation expectations decline. Despite the general gloom, the central bank is clearly giving renewed confidence in Hungary’s prospects to international investors, who recently happily snapped up a €1 billion government bond issue. The central bank’s swift action to prevent a banking crisis last fall and its acceptance of assistance from the IMF have probably also contributed to Hungary’s rapid rehabilitation.

Norway

Norway

Svein Gjedrem

Grade: C-

When everything was going smoothly for Norway, its central banker, Svein Gjedrem, appeared to have a confident and skilled grip on the levers of monetary control. As the waves of global turmoil have buffeted Norway in the past two years, though, Gjedrem has begun to look increasingly clumsy and flat-footed. The central bank correctly predicted that inflation was poised to surge last year but bumped up interest rates too late to prevent it happening. As a result, while the global slowdown was becoming more apparent last year, Norges Bank was still tightening monetary policy in an attempt to wrangle inflation back down below a decidedly uncharacteristic 5%. In October it performed an abrupt volte-face in response to the growing threat of economic contraction. By June this year the bank had slashed interest rates from 5.75% to a record low of 1.25% in what many have characterized as a belated attempt to prevent the country’s non-oil economy skidding into recession. The shock therapy did not prevent Norway’s mainland GDP from shrinking and has left the central bank looking reactive and unpredictable. Long admired for its openness and clarity, the central bank is suddenly sounding much less self-assured while Gjedrem himself all but admitted in August that the bank really does not have a clue which direction monetary policy will take next.

Poland

Poland

Slawomir Skrzypek

Grade: B

Slawomir Skrzypek was criticized across the board before the global financial crisis hit for failing to hike interest rates fast enough to contain inflation. Skrzypek’s defense was that Poland’s ongoing economic slowdown would tame inflation without the bank having to lift a finger—a conviction that turned out to be remarkably prescient. With inflation edging lower, in fall last year the bank embarked on a long series of interest rate cuts aimed at stimulating the stumbling Polish economy. Unfortunately, a concurrent sharp slide in the zloty’s value put pressure on import prices, and inflation again surged above the central bank’s 3.5% upper target before edging slightly lower in July. Despite the concerns about inflation, the central bank has made it clear that it does not expect any significant changes for the rest of this year in the record-low 3.5% base rate. Skrzypek remains bullish, claiming that inflation will return to the bank’s target of 2.5% by mid-2010 while GDP growth should recover sooner than expected; in June he predicted that Poland would see 1% GDP growth over the full-year 2009. Given his record, his critics are likely to give him the benefit of the doubt this time around.

Russia

Russia

Sergei M. Ignatiev

Grade: C-

Compared to his counterparts overseeing other major economies, Sergei Ignatiev, Russia’s central banker, has been practically invisible during the recent market upheaval. In a rare public appearance in March this year, Ignatiev said only that the central bank had been “proactive” in tackling the banking crisis in Russia and that it would continue to focus on gradually reducing inflation, despite the multi-billion-dollar stimulus injected into the economy by the central bank and the Russian government. The bank has certainly been active, if not necessarily proactive. As it became clear that Russia would not escape the fallout of the credit crunch and that its somewhat fragile banking system could be at risk of collapse, the bank opened the liquidity floodgates. But, like many central bankers, Ignatiev found himself caught between the need to loosen monetary policy to prevent a banking system collapse and the incipient threat of inflation. He was saved, to an extent, by slumping oil prices, which helped ease inflation pressure. Unfortunately, slumping oil prices also contributed to a run on the ruble that had been triggered by a flood of hot money leaving the country in search of less-risky investments. The bank drew heavily on its ample foreign exchange reserves in a vain attempt to shore up the ruble before it accepted the inevitable and allowed the currency to slide. Despite the bank’s near-$200 billion intervention, the ruble ended up slumping by a third against the dollar, although it has recovered slightly since the first quarter of this year.

Czech Republic

Czech Republic

Zdenek Tuma

Grade: A

In common with many of his peers, the Czech Republic’s central banker, Zdenek Tuma, underestimated the depth of the recession his country would endure this year. Unlike many of his counterparts, though, Tuma did respond to the imminent economic slowdown and began trimming interest rates in August last year. With inflation at a lofty 6.9% it was a bold move, but one that proved successful. Although annual GDP this year is expected to shrink by almost 4%, the bank believes growth has already turned positive and should remain so for the foreseeable future. Tuma’s decisiveness and willingness to make sharp, repeated cuts to interest rates almost certainly helped reduce the impact of the global slowdown on the Czech Republic. However, with interest rates already at a low of 1.25%, Tuma has limited room for maneuver, so he will be hoping his cautiously optimistic growth forecast proves accurate. With inflation close to zero and showing no signs of leaping higher, despite the low interest rates, Tuma is confidently predicting that he will not have to raise rates until at least the second half of 2010. The darkest cloud on the horizon is the continued strength of the Czech crown, which remains one of the strongest currencies in the region.

European Union

European Union

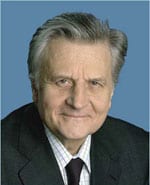

Jean-Claude Trichet

Grade: A

Always prone to plowing his own furrow, European Union central banker Jean-Claude Trichet has really shown his mettle in the past year. Turning a deaf ear to the cacophony of calls for drastic interest rate cuts in response to the past year’s economic turmoil, Trichet carefully crafted the euro area’s monetary policy to contain inflation while still pouring liquidity into its ailing banking system. His “gradualist” approach is criticized by many who complain that he is behind the curve in tackling the region’s economic turmoil, but, says Trichet, that is exactly the point. By taking a measured approach and avoiding sharp, reactive changes in policy, the bank helps smooth out rather than amplify the peaks and troughs of economic activity in the region. Predictably, as Europe’s economic fortunes appear to be reviving, Trichet is under pressure to shut down the ECB’s cheap money supplies, and, true to form, the central banker is unmoved. Wary of stunting the recovery before it is fully established, Trichet promises to keep monetary policy loose for some time to come. He has also made a point of reminding policymakers around the world that the financial system is still in need of significant reform—something that many might be forgetting as the recent fears of a global financial meltdown fade.

Sweden

Sweden

Stefan Ingves

Grade: C-

Until very recently, Sweden’s economy was whirring along nicely, fueled by a successful and internationally adventurous financial services industry and buoyant high-end consumer durables exports. Then the credit crunch hit, and after years of steady growth and low inflation, the country has found itself with a shrinking economy, unpredictable inflation and a decidedly volatile exchange rate. As the IMF recently commented, “Having surfed the earlier global wave, Sweden has been hit hard by its crash.” Among those left gasping for breath on the beach was Stefan Ingves, Sweden’s central banker. Seemingly oblivious to the economic tsunami heading Sweden’s way, Ingves was still tightening monetary policy last fall, cranking rates up to a 12-year high of 4.75% in September. In October Ingves did an abrupt about-face and by the end of the year had slashed rates to 2%. Early this year the central bank admitted that Sweden’s economic pain was far worse than it had expected and halved rates to 1%. By mid-July it had halved rates twice more to leave them at just 0.25%. With growth still anemic, inflation well below the bank’s 2% target and unemployment set to peak at 11%, Ingves is now left with little option but to cross his fingers and hope for the best.

Switzerland

Switzerland

Jean-Pierre Roth

Grade: B

Switzerland’s central bank has been much busier than usual of late. As well as dealing with the imported problems from the global credit crunch and subsequent widespread economic downturn, the Swiss National Bank has been busy rescuing one of the country’s flagship banks, UBS. With characteristic understatement, Swiss central banker Jean-Pierre Roth described the purchase of a 9% stake in UBS as helping the embattled bank with its “credibility problem.” Not long afterward, the SNB was dealing with a credibility problem of its own as it admitted the country’s economy was in recession and facing the specter of deflation for the full-year 2009. By March this year the bank had slashed interest rates to near zero, was pumping liquidity into the system and had risked global opprobrium by intervening in the forex markets to bring down the soaring franc—but the outlook was as gloomy as ever. Roth has grumbled before that the franc’s status as a safe-haven currency limits the efficacy of the SNB’s monetary policy, and recent events have clearly borne this out. Until the global flight to safety truly abates and investors start selling their francs as they seek higher-yielding investments elsewhere, Roth will be saddled with an overvalued currency and an underperforming economy.

Turkey

Turkey

Durmus Yilmaz

Grade: B

Turkey’s central bankers always appear to be locked in a battle with inflation, and Durmus Yilmaz is no exception. His record on that front is not exactly stellar, as inflation consistently overshot the central bank’s targets for several years. This past year, though, Yilmaz appears to have hit his stride. Confident that the global slowdown would squeeze Turkish inflation down sharply, Yilmaz embarked on a dramatic round of interest rate cuts in November last year. By February he had slashed rates from 16.75% to 11.5%, following up in April and August with further cuts that brought the bank’s key rate to 9.5%. Gratifyingly, Yilmaz’s conviction that inflation would subside despite the sharp rate cuts proved correct, and he now believes that by year-end it will have sunk to 5.9%, while there are already signs that Turkey’s economy, boosted by the lower interest rates, could be emerging from the slump. By the end of 2010, Yilmaz is predicting inflation will be down to 5.3%. Both figures are comfortably below the bank’s upper target levels. Yilmaz deserves credit for his outspoken efforts to persuade the Turkish government to exercise fiscal restraint. He has also urged the country’s leaders—in no uncertain terms—to implement the structural reforms necessary to bring Turkey in line with the EU accession criteria.

United Kingdom

United Kingdom

Mervyn King

Grade: B

A year ago it was touch and go whether Mervyn King would remain as the governor of the Bank of England. In the end he managed to swing another five-year term but not before he was hauled over the coals for failing to save the United Kingdom from recession, failing to keep inflation below target and failing to prevent Northern Rock from failing. What King’s critics failed to appreciate was that all those failures were linked, and it would have been practically impossible for King not to fail—at least on one count, if not all. Luckily for King, it turned out that the UK was the bellwether for the developed markets generally, most of which were diving into their own death spirals before the ink was dry on King’s letter of reappointment. Perhaps chastened by allegations that King tended to do too little, too late, the bank then lurched ahead of the curve, joining the vanguard of central banks driving interest rates down to near zero and indulging in so-called quantitative easing. The bank’s belated boldness appears to be doing the trick. It now predicts that growth will recover in 2010 while inflation will remain around or below the 2% target for some time to come.

Asia

China

China

Zhou Xiaochuan

Grade: C

Last year the People’s Bank of China (PBOC) appeared to be reluctant to tighten the monetary policy reins. This year, however, it appears to be slowly starting to turn the screws. The PBOC has made it clear it needs to keep a watchful eye on the spate of new lending activity by banks, which in the first few months of this year was almost three times the 2008 level. New lending has had the desired effect in terms of propping up spending and has kept projected real GDP growth for this year and next at a buoyant 8%. However, there are concerns that the economy may overheat and non-performing loans (NPLs) will increase. With new loans still increasing in June, banks did not appear to be heeding the PBOC’s call for restraint. It is questionable whether the bank can forestall a credit bubble at the same time as maintaining its relatively loose monetary policy stance. There is also the nagging question about the valuation of the renminbi, which, according to some economists, is undervalued by 15%-25%. With exports driving the country’s continued economic growth, though, China is unlikely to want its currency to appreciate.

India

India

Duvvuri Subbarao

Grade: B

India expects to turn in a chunky 6.7% increase in GDP this year, but all is not rosy. Inflation is stubbornly refusing to budge from its 6% average this year, and there are concerns that the central bank’s efforts to combat the credit crunch by boosting liquidity will only add to inflationary pressures. Duvvuri Subbarao, who took over as India’s central banker last year, has been pumping liquidity into the system by reducing the cash reserve and statutory liquidity requirements for banks, as well as providing a special refinancing facility for banks. These measures appeared to have worked, increasing the availability of credit but not to excessive levels. However, government stimulus packages have raised the fiscal deficit, which is projected to reach 6.8% in 2009-2010. Subbarao is mindful of the need to prevent excessive government borrowing while also ensuring ample liquidity is available to meet private sector demand, and he has demonstrated his willingness to tighten and loosen monetary policy as needed. While adopting a more accommodative stance in the wake of the financial crisis, Subbarao has hinted that his “expansionary policies” could be reversed in the near future as the economy shows demonstrable signs of improvement.

Australia

Australia

Glenn Stevens

Grade: A

With GDP set to contract only slightly in 2009 and inflation predicted to hit a modest 1.6% for the year, it looks like Glenn Stevens’ policy of “aggressive” loosening of the overnight cash rate has worked like a charm. Some observers suggested that Stevens overreacted to the global and domestic downturns, having slashed rates by 425 basis points between March 2008 and April 2009. However, he is one of the few central bankers who both spotted the crisis on the horizon and actually did something about it before it was too late. With the key interest rate now at 3% and inflation prospects looking remarkably benign, the bank claims it has room for further cuts if necessary. Recent data, however, suggest that the next move is more likely to be up than down. The bank admitted it was surprised by the recent signs of recovery and is ready to tighten policy if it senses that the economy really is out of the woods. Slashing the cash rate has also had a positive impact on Australia’s household debt problem. In December Stevens indicated that rate cuts meant that “the fall in the household sector’s gross debt-servicing burden [would] be almost 3% of household income.”

Indonesia

Darmin Nasution (acting governor)

Grade: Too early to say

Boediono’s tenure as governor of Bank Indonesia was short lived, as in May, just a year after he took office, he was accepted as a candidate for vice president of Indonesia. However, he is no doubt responsible for recent gyrations in interest rates at the bank. Last year, with inflation soaring, the bank pushed up rates to 9.5% before instituting a series of rate cuts as inflationary pressures declined. By the end of the first half of this year inflation was down to 3.7% despite the 3 percentage point fall in central bank interest rates. Cognizant of the inflationary effect of lower interest rates, the central bank predicts that price increases will grow next year and has already announced that it expects to tighten monetary policy in the near future. While inflation seems under control and GDP is still expected to grow this year, economists say the rate cuts have had little impact on bank lending, with bank credit growth declining. However, some analysts have revised upward their forecasts for real GDP growth this year to 2.6% following a surprising 4.4% year-on-year growth in real terms in the first quarter. At its September meeting, the bank opted to keep rates unchanged at 6.5%, citing its belief that the appreciating currency is offsetting the slight upward trend in inflation.

Japan

Japan

Masaaki Shirakawa

Grade: B-

Masaaki Shirakawa took the reins at the Bank of Japan at a difficult time. After spending years battling deflation, the bank last year suddenly was facing the threat of inflation. With interest rates effectively at zero, the bank had plenty of scope to tighten monetary policy, but for one thing: Growth was slowing at the same time, and the last thing the bank wanted to do was to accelerate Japan’s slide into recession. In the end, it did practically nothing, and, as it turns out, it appears that Japan’s doughty economy is going to pull through. According to the bank, if general global growth resumes and there are no significant shocks to the domestic or foreign markets, Japan should return to a normal economic environment with steady growth and stable prices. Under the current circumstances, that is an awfully big “if,” and Shirakawa knows it. He admits that business investment and domestic consumption remain weak and that unemployment is worsening. He also knows that preventing a “deflationary spiral” is the biggest battle he faces, but he is hopeful that providing banks with sufficient liquidity, combined with a low-interest-rate environment, will have a positive impact on corporate funding and the wider economy in general.

Malaysia

Malaysia

Zeti Akhtar Aziz

Grade: A

Malaysia’s economy has suffered over the past year, with GDP contracting 6.2% year-on-year in the first quarter as the country’s export market suffered from the fall in global demand. At the same time, though, increases in food prices have tailed off. The central bank forecasts average annual inflation to settle between 1.5% and 2% this year. As inflation has fallen, Zeti has adopted a measured approach to loosening monetary policy, with 150 basis points in rate cuts from last November to March this year. For the moment, she is holding off any further easing as growth is expected to return in the latter half of the year. The bank’s key rate is expected to remain at 2% for the remainder of the year and into 2010. Meanwhile, Zeti has turned her focus to other monetary policy measures for stimulating growth: ensuring that the central bank’s rate cuts are being passed on to borrowers and that there is ample liquidity swilling around in the system for companies that need refinancing. However, she needs to remain vigilant to ensure that promoting bank lending does not generate more non-performing loans.

New Zealand

New Zealand

Alan Bollard

Grade: C

The Reserve Bank of New Zealand has demonstrated its resolve in its fight against the recession. From July last year up until April this year, central banker Alan Bollard has considerably loosened monetary policy, slashing rates progressively from 8.25% to 2.5%. By June it appeared the cuts were working, as a slight uptick in household spending and investment prompted the bank to hold rates steady at 2.5%. Bollard believes the rebound in spending may not be sustainable, though, given that unemployment remains high and households are nursing high levels of debt. With risks to economic activity remaining on the downside, Bollard may need to ease monetary policy even further. The outlook is not helped by a recent appreciation of the New Zealand dollar after it had fallen dramatically in the wake of hefty interest rate cuts. Bollard will need to take decisive action when it comes to further rate cuts, which he has not ruled out. He is treading a fine line, though. Inflation remains within the bank’s target range, but Bollard may need to become more hawkish going forward, given the potential pitfalls of easing monetary policy too far.

Philippines

Philippines

Amando M. Tetangco Jr.

Grade: B

In June last year inflation in the Philippines reached a 14-year high of 11.4% year-on-year, and the central bank admitted that full-year 2008 inflation was set to burst above the bank’s 4% target. Amando Tetangco responded by tightening monetary policy, nudging up rates between June and August by a total of 1 percentage point. By October, though, it was becoming clear that external factors were helping to rein inflation in and that the bigger near-term threat was declining GDP growth. Again, Tetangco took a measured approach, easing interest rates down by 2 percentage points over the following nine months and loosening requirements on bank lending in an attempt to maintain liquidity in the financial system. The central bank governor obviously believes he has done enough for now to temper inflation and to reduce the cost of borrowing to help stimulate the economy, which is expected to contract by 1% this year. While inflation is projected to rise again later in the year, Tetangco expects it to remain within the central bank’s target range. However, it is clear that inflation targeting will be the governor’s main preoccupation, and it will dictate when the central bank moves to a less accommodative stance on monetary policy.

Singapore

Singapore

Heng Swee Keat

Grade: B

Heng Swee Keat has had a difficult year. As one of the most trade-oriented economies in the world, Singapore was hit hard by the global slowdown. Analysts predict that real GDP could contract by as much as 6% this year. The central bank itself has said GDP could fall by as much as 9% over the course of 2009, while inflation will slump to zero—or possibly lower. Not surprisingly, the central bank’s monetary policy is expected to remain loose. However, Heng will need to be careful that further easing does not cause the Singapore dollar to become too weak, given that the bank’s main monetary policy measure is targeting the exchange rate. In October last year the central bank adopted a 0% appreciation stance of the Singapore dollar, which it has maintained in order to avert further volatility. The city-state may be about to change course in its monetary policy, though, as recent figures have shown GDP growth exceeded expectations. Heng has also worked hard in the past 12 months to strengthen the financial system, shoring up liquidity with revisions to its Standing Facility, forging linkages with other central banks and closely supervising local banks.

South Korea

South Korea

Lee Seongtae

Grade: A

South Korea was among the worst hit by the global economic slowdown, with the Korean won depreciating up to 43% against the dollar and exports falling by 34% year-on-year. Lee Seongtae has worked hard and swiftly to restore stability to the banking and foreign exchange markets, instituting a range of measures such as expanding the provision of liquidity via open market operations and lending facilities as well as providing foreign currency liquidity to domestic financial institutions. So far the liquidity provisions appear to be working, with the forex markets showing signs of improvement and the Korean won rebounding. However, having been through such a difficult year, Lee recognizes the need to remain vigilant. He has also resorted to more conventional monetary policy measures such as lowering the base rate by 3.25 percentage points to a record low of 2%. He is unlikely to push it down further as inflationary pressures remain ever present. So far, slashing the base rate appears to have had the desired impact on bank deposit and lending rates. Lee remains accommodative in his outlook and does not rule out further rate cuts if conditions worsen.

Thailand

Thailand

Tarisa Watanagase

Grade: C

Three years into the job, Tarisa Watanagase appears to have developed considerable confidence in her role as Bank of Thailand governor, having raised the ire of the government last year by increasing interest rates at a time when political leaders were trying to stimulate economic growth. This year, however, Watanagase’s stance has been more accommodative, with the policy interest rate being cut from 3.75% last December to 1.25%. Watanagase will be frustrated that the cuts have had little impact on the real economy in terms of loan growth. No surprise, then, that she has kept rates on hold as she waits to see if future economic data provide some glimmer of hope that the cuts have filtered through. However, with rates so low, she has left herself little room to maneuver. For the first time since the 1997 Asian economic crisis, the Thai economy is expected to shrink—by between 3.5% and 4.5% this year—with growth returning in 2010. Some encouraging signs appeared in the second quarter with rising exports and lower unemployment figures. However, private consumption and investment still remain at low levels.

Taiwan

Taiwan

Fai-Nan Perng

Grade: A

Taiwan’s central bank acted faster and more decisively than many of its peers last year as it saw its country’s export volumes falling. In September the bank began loosening the reins on monetary policy, cutting the base rate over several months by 2.375 percentage points to 1.25%. Although analysts were expecting further rate cuts at the bank’s meeting in March, the country’s central banker, Fai-Nan Perng, has kept a cool head, maintaining the base rate at 1.25%, implying that he believes he has done enough for now in terms of loosening monetary policy to try to improve the economic outlook. Any further cuts to base rates are likely to result only in marginal improvements, and exports have already recovered slightly from last year’s downturn. Inflation also remains at a low level, so for now it seems prudent that the central bank keeps any future rate changes on hold until economic or inflationary data suggest it should consider doing otherwise.

Middle East & Africa

Israel

Israel

Stanley Fischer

Grade: A

For a small, open economy like Israel, the central bank needs to make sure that an overvalued currency is not negating the effects of low interest rates. Stanley Fischer implemented an aggressive currency intervention policy at the Bank of Israel that pushed the country’s international reserves in July 2009 up to a record $52 billion, double the level of a year earlier. Fischer, former deputy managing director at the International Monetary Fund, saw the global recession coming and helped to limit its effect on the country’s exports by buying dollars and selling shekels to restrain the currency’s advance. In August 2009 the central bank ended its daily purchases of dollars, which had reached $100 million on a regular basis, and announced that it would continue to intervene to counteract disorderly market conditions. The element of surprise helped to discourage hot-money inflows, with daily intervention of as much as $500 million at times. The Bank of Israel surprised the markets a second time in August when it became the first major central bank to raise interest rates since the financial crisis worsened in September 2008. While the quarter-point increase from a record-low 0.5% came sooner than most analysts expected, it struck a balance between the need to control inflation and to support the country’s budding economic recovery.

Saudi Arabia

Muhammad Al-Jasser

Grade: C

Muhammad Al-Jasser was named in February 2009 to head the conservative Saudi Arabian Monetary Agency (SAMA), the kingdom’s central bank. The former deputy governor was well schooled in SAMA’s strict regulatory policies. Long used to cautioning banks about the dangers of speculation, he faced an entirely different problem when commercial bank lending seized up in the face of a weak economy. Like other central banks around the world, SAMA cut rates. Commercial banks were afraid to lend, however, in part because of worries about the problems at two family-owned conglomerates, Saad Group and Ahmad Hamad Algosaibi & Brothers, which announced plans to restructure billions of dollars of debt. SAMA was silent about the extent of the problem, which may have exacerbated the lack of trust in a system that lacks transparency. Al-Jasser was right to maintain the riyal’s peg to the dollar during these uncertain times. However, he may have undermined efforts to advance monetary union in the Gulf with his insistence that Riyadh host the forerunner of the Gulf Cooperation Council’s proposed central bank. The move was not well received in the United Arab Emirates, the second-largest economy in the GCC, which opted to pull out of the project.

South Africa

South Africa

Tito Mboweni

Grade: B

Tito Mboweni’s days are numbered as governor of the Reserve Bank of South Africa. Gill Marcus, chairperson of Absa, one of South Africa’s leading banks, will take his place come November 9. If former A-grade-winner Mboweni can be faulted, it is for sticking to a tight monetary policy to combat inflation at a time when the economy was clearly faltering. While Mboweni was reappointed as Reserve Bank governor before indicating his desire to leave the post, he likely would have clashed eventually with Jacob Zuma, the populist leader of the African National Congress, who was elected president of South Africa in April. Marcus could abandon inflation targeting to boost the economy, but her banking experience and former positions as a deputy governor of the Reserve Bank and deputy minister of finance have reassured investors. They remain nervous, nonetheless, that Mboweni may have failed in his goal of preserving the unquestioned independence of the central bank.