New capabilities are bringing speed to banking while simultaneously expanding access. Global Finance recognizes outstanding innovations in local and regional markets around the world.

This year’s outstanding innovations by category, were often built by banks in collaboration with third parties, have taken advantage of digital technologies, including artificial intelligence, big data and application programming interfaces to deliver digital banking solutions that tap into their customer’s very specific needs.

From targetted banking solutions for young people to underserved small-to-medium-sized (SMEs) enterprises the winners have adopted new services and personalized journeys that cover everything from easier access to financing, improved treasury solutions, access to Environmental, Social, and Governance metrics, financial inclusion, digital onboarding and fraud detection. The unprecedented rise in e-commerce, meanwhile, has led to greater emphasis on user experience – offering improved user interfaces to consumers, SMEs and corporate clients.

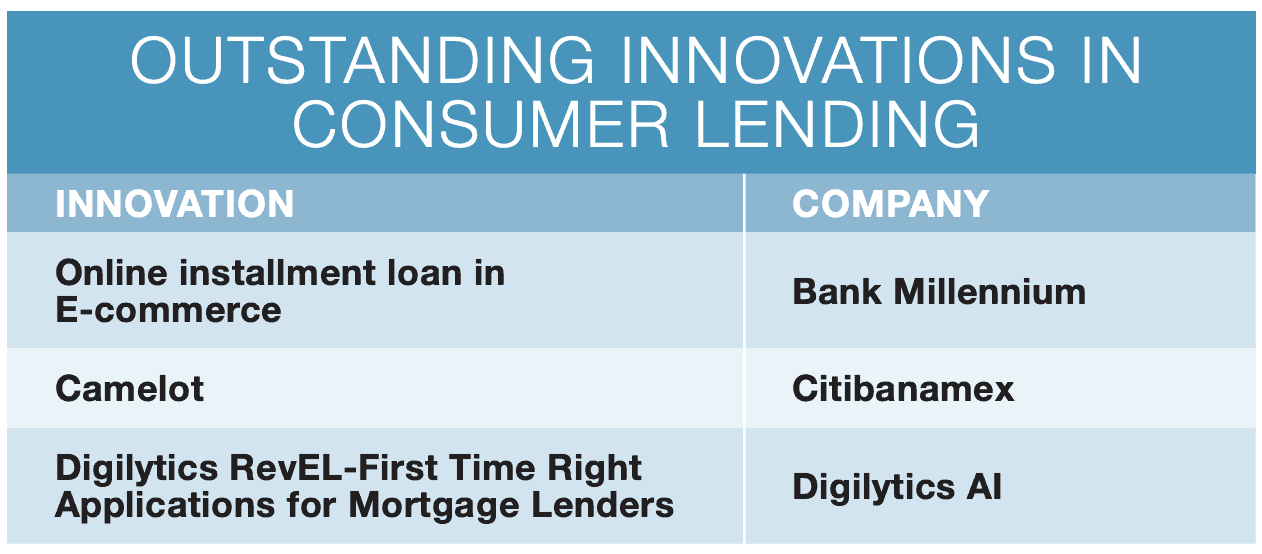

Online installment loan in e-commerce

Bank Millennium’s online installment loan is offered in appliance and electronics stores through its open-banking solution. Once customers confirm their identity by logging into their bank account, they complete an application form that asks for certain financial data (liabilities may be sourced from credit bureaus). As soon as they submit the form, they receive a credit decision in real time. This innovative service of quick credit decisions is offered in eight Polish banks. Customers can access the form from the banks; websites, and the form is adaptable to any device. The process for customers was designed to be simple and user friendly. Once approved, the customer signs the form with an SMS password.

Camelot

Citibanamex’s Camelot uses artificial intelligence (AI) to expand access to loans—incorporating a reliable employment-stability prediction into credit decisions grew loan eligibility for the bank by over 30%. Citibanamex’s advanced analytics consider attributes like industry-specific employment cycles, and has demonstrated that employment stability determines credit performance as much as or more than traditional data. This was the first time a machine-learning model was used to automate data ingestion and scoring, and Citibanamex used its big data platform and application programming interfaces (APIs) to model the data without any manual intervention.

Digilytics RevEL

Digilytics AI’s Digilytics RevEL is the first of its kind to use AI to process mortgage applications with over 95% accuracy. Traditionally, borrowers have physically submitted applications with supporting documentation; then the lender manually checked the application for accuracy. Digilytics RevEL uses AI, machine learning and other advanced techniques to automate the mortgage-origination process by extracting and verifying borrower information and then delivering accurate applications. This product eliminates nonvalue manual tasks and augments decision-making. By automating parts of the loan-origination process, lenders can make decisions on loan approvals faster.

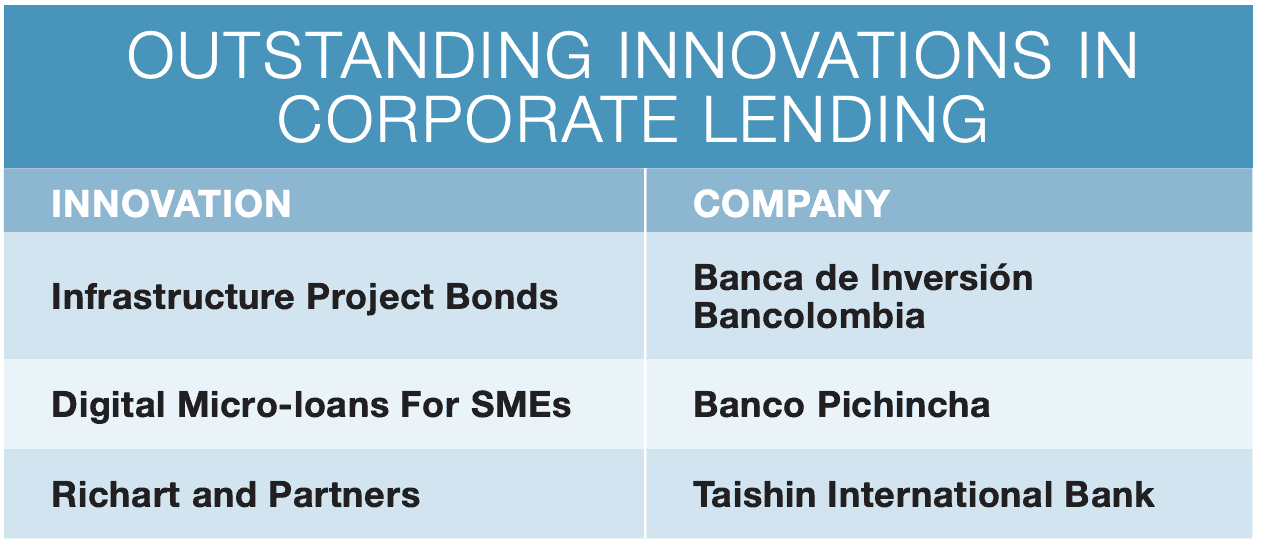

Infrastructure project bonds

Banca de Inversion Bancolombia issued the first infrastructure project bonds in Colombia, in the amount of 700 billion Colombian pesos (about $176 million). Projects had traditionally been funded with local and international debt, and this issuance created new financing opportunities in the market, providing institutional investors new to the project finance sector with access to a new financing instrument. As this was a first-time issuance in Colombia, the bank educated investors about the product’s structure and tailored the timeline to meet investor needs. The clients were the Tunel Aburra Oriente Concession Trust and its shareholders, and the transaction was used for debt reprofiling and shareholders’ dividend recapitalization.

Digital microloans for SMEs

Much of Ecuador’s banked population doesn’t use digital banking tools. While microentrepreneurs have used digital tools at an increasing rate since the start of the pandemic, they did not have a process for obtaining loans without a cumbersome underwriting process. Banco Pichincha developed digital microloans for small and midsize enterprises (SMEs), the first 100% digital solution for Ecuador’s small businesses. This new digital tool gives microloans to small entrepreneurs in five minutes without the need for gathering information, controlling the methodology and recovery, and providing additional financial education to the borrowers.

Richart and partners

Taishin International Bank developed the Richart IDEA (Intelligent Delivery API) module, the first cross-industry collaboration in Taiwan finance. Partners can customize this API for their specific business processes and eliminate pain points between consumers and other partners. Customers purchasing in groups can now use a chatbot called Richart’s Split Together that automatically divides payment. To facilitate payments between tenants and landlords, the API interfaces with DDRoom’s website, with Richart automatically executing the transaction. The API integrates with FamiPort+ to integrate loans with e-commerce sites, so that consumers can easily finance purchases. Finally, Richart partnered with music streaming service KKBox. Now, when consumers buy a time-deposit service, they can choose between the interest payments and music services.

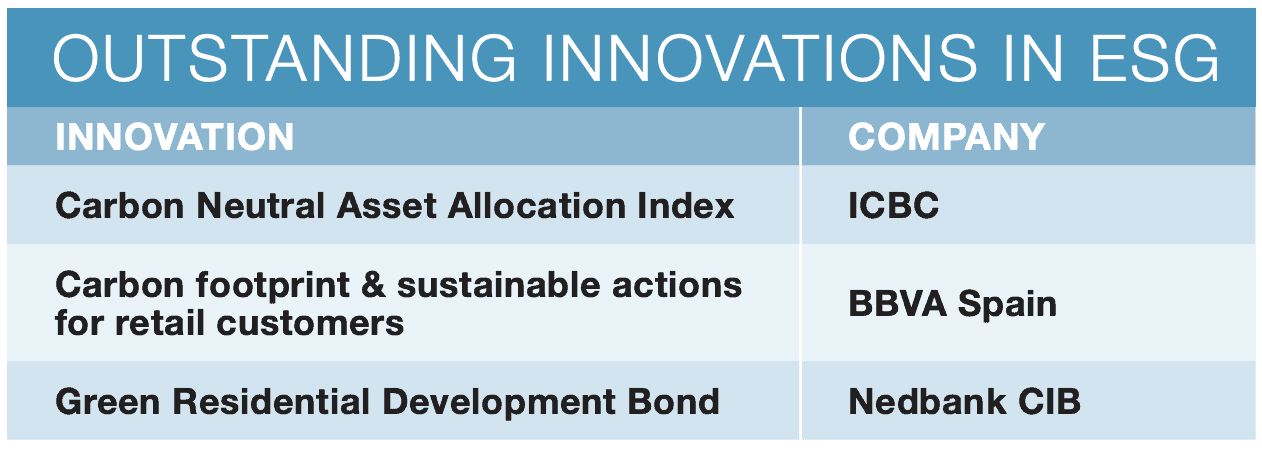

Carbon footprint and sustainable actions for retail customers

BBVA Spain’s Carbon Footprint calculator, the first such calculator offered by a bank in Spain, is one of the first globally to use transactional data of retail customer accounts and cards to detail the origins and size of customers’ emissions.

Carbon neutrality asset allocation index

The transition to net zero is even more challenging in countries with a heavy reliance on fossil fuels. ICBC in China devised its Carbon Neutrality asset allocation index to encourage investment in green development. It is the first carbon-neutrality themed index jointly launched by a wealth management subsidiary and China Securities Index, and also the first carbon-neutrality themed multiasset index in the Chinese market. Encompassing 220 stocks and more than 260 bonds, the index incorporates more than 30 segments of high-carbon-emission reduction.

Green residential development bond

In Africa, the green residential development bond of Nedbank CIB (Corporate and Investment Banking), listed on the Johannesburg Stock Exchange in December, was the first of its kind in Africa. Funds will finance residential developments constructed with the Excellence In Design Green Efficiencies standards of the International Finance Corporation (IFC). The bond blends a unique mix of financing sources: an anchor investment of more than $300 million from the IFC; and a $2 million performance-based incentive provided by an IFC-UK government donor-funded program called Market Accelerator for Green Construction.

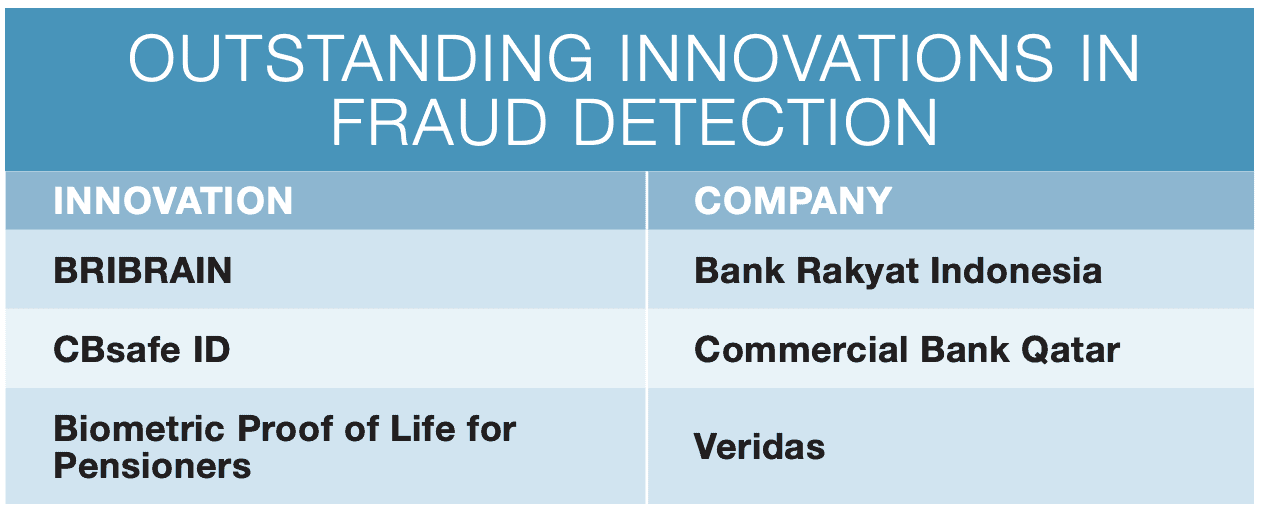

BRIBrain

BRIBrain is the first and largest neural network in the microfinance sector, and the AI-powered big data platform of Bank Rakyat Indonesia (BRI). By leveraging this platform, BRI can reach the smallest segments of the market and this innovation is helping BRI become a hybrid bank with digital services. BRIBrain is built with BRI’s data lake, containing over 30 years of inputs, and uses machine learning and AI to improve the bank’s risk management. The neural network focuses on four areas—credit scoring, merchant assessment, customer profiling and fraud detection—and provides insights to the bank’s processes for savings, lending, security and businesses.

CBsafe ID

To protect customers against fraud, Commercial Bank Qatar launched CBsafe ID, the first customer digital security service in the region. Before a bank’s agent calls, customers receive a push notification on their mobile device to inform them the bank is about to call. So the agents can confirm their identity when they call, they tell customers the CBsafe ID number that’s in the mobile banking app, reducing the chances of being tricked.

Biometric proof of life for pensioners

Senior citizens collecting pensions in Mexico need to provide proof of life by physically going into a bank office every six months, which can be difficult as few branches are available for this service. Veridas can now verify a person’s identity with a single 3-second call at any time, from any place, in any language or dialect, after they have made a single visit to generate a voiceprint. Veridas’ voice recognition system can compare multiple voices and detect recordings to prevent identity theft and fraud.

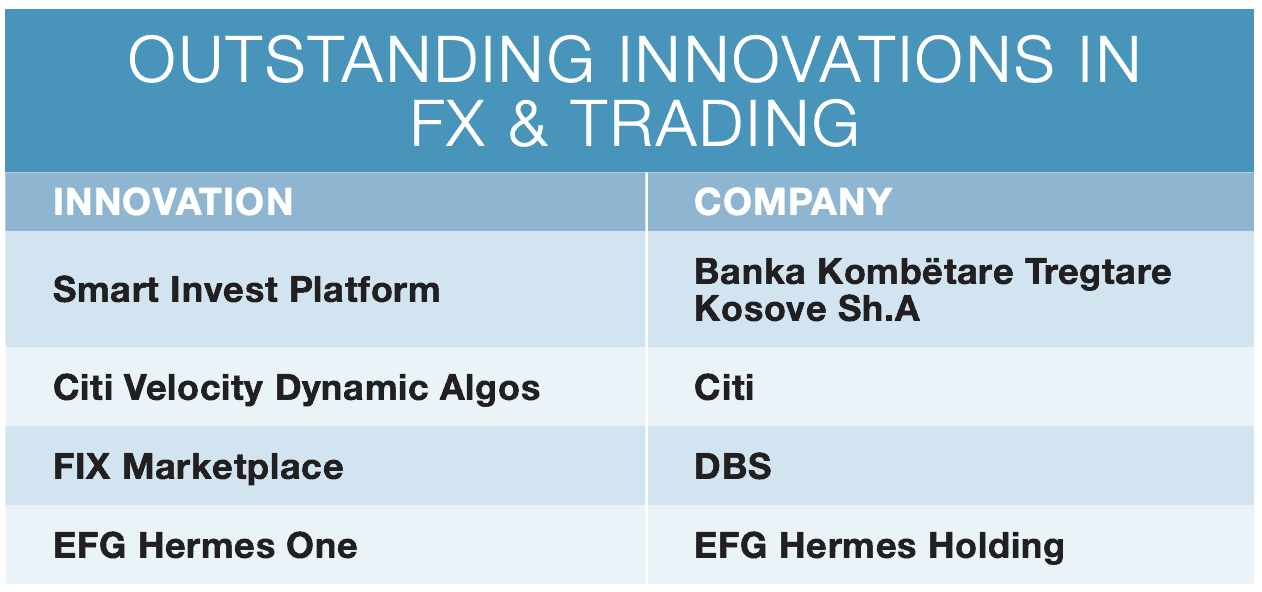

Smart Invest platform

Introduced during the pandemic by Banka Kombetare Tregtare Kosove, Smart Invest is the first online platform in Kosovo that allows clients to make investments globally, providing direct access to foreign exchange (FX), commodities and stocks in the US, Germany, Japan, the UK, South Africa, Peru and many other markets. Unlike a traditional investment brokerage that requires phone and email requests during office hours, Smart Invest enables clients to close positions whenever they deem necessary and withdraw funds as soon as they exit position. Clients can perform one-click investments on their phone, access related news, receive alerts and notifications, and subscribe to a daily financial bulletin in the Albanian language.

Citi Velocity Dynamic Algos

In 2021, Citi rolled out Citi Velocity Dynamic Algos, a futures algorithm platform that includes time-weighted average price, volume-weighted average price and more; and Arrival, an implementation shortfall algorithm, across all major exchanges in the US, Europe and Asia-Pacific. Citi says it offers clients “a dynamic suite of strategies allowing them to pursue optimal execution with minimal market disruption,” by giving clients maximum control over the way their algorithm responds to live market conditions. An enhanced transaction cost analysis (TCA) tool includes functionality such as live algorithm tracking and periodic fill rate analysis. By building algorithms specifically for listed derivatives, Citi caters to the unique characteristics of these diverse instruments and their market microstructures.

FIX Marketplace

Launched in June 2021, DBS’ FIX Marketplace is the first fully digital and automated fixed income execution (FIX) platform on which bond issuers can directly connect with investors in Asia. The platform is part of the Singapore-based bank’s strategy to digitalize Asia’s capital markets. It empowers issuers with the ability to tap capital markets in a manner that saves time and money, while also providing more-inclusive and -accessible markets for issuers. Following a few simple steps, and with no involvement of the bank, issuers can launch new deals on the platform. Full digitalization enables direct order-taking and transparent allocation on primary market bond issuances, allowing digital end-to-end self-executing trades from issuers and investors subscribing to these trades directly on the platform.

EFG Hermes One update

In 2021, EFG Hermes launched an advanced version of its flagship EFG Hermes One trading platform—enabling both new and veteran investors to tap into investment information, execute informed trades and monitor their portfolios in real time. A new Learn tab opens access to EFG Hermes Research, while EFG Hermes One Virtual Simulator allows them to simulate the trading experience on the application to build skills prior to trading. With a plethora of new services, including margin trading, short selling, same-day and second-day trading, access to IPOs and much more, the new app also has a fully digitized onboarding process and a digital payment gateway; and it boasts a new and improved user interface.

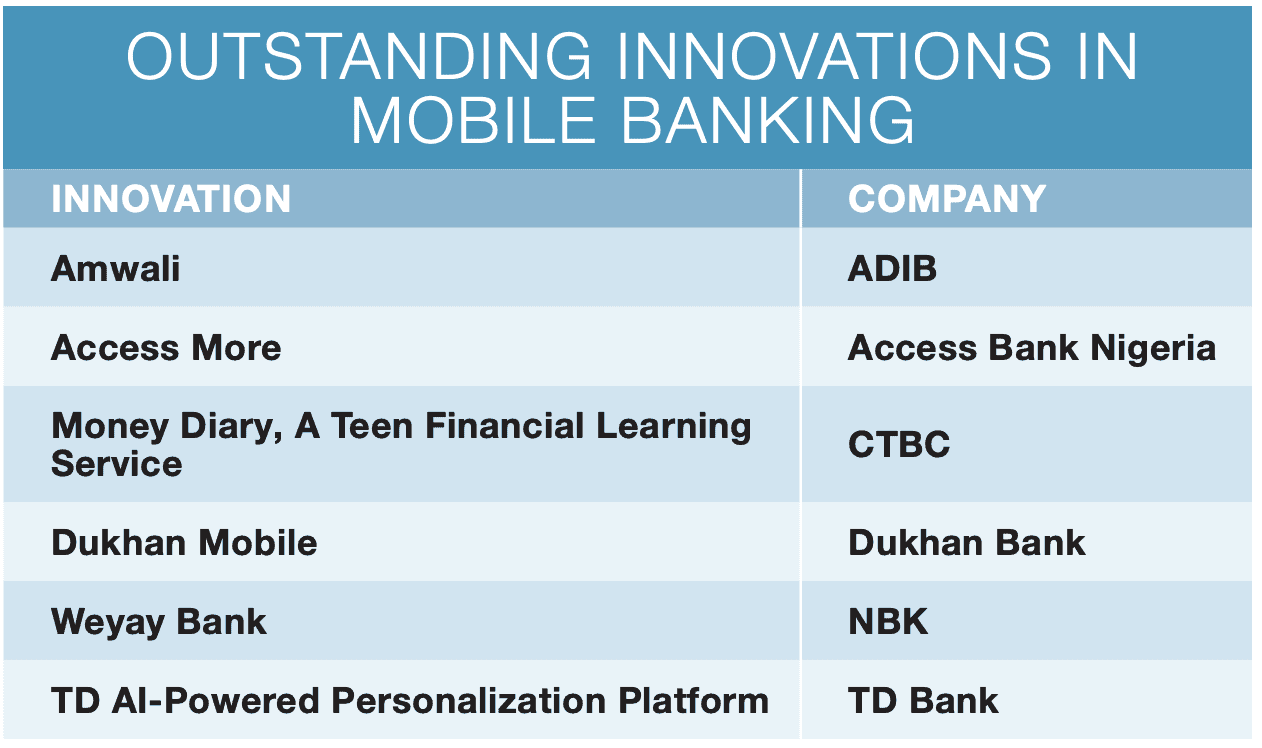

Access More

Access More is a lifestyle and payment app with Bluetooth payment features, including QR, face pay, Access Rewards, fast pay, flight booking, Visa payments and instant loans. Launched in 2020, the Access More app is the first all-inclusive payment and lifestyle super app in Africa. Access Bank’s aim to enhance digital inclusion through gamification and incentivization (Access Rewards) resulted in several successful campaigns throughout 2021, whereby cash and gift prizes were awarded to Access More users during campaigns. Access Bank is extending the app to Kenya, South Africa, Zambia and other African countries, to provide a universal payment gateway connecting Africa to the world.

Amwali

Amwali, from Abu Dhabi Islamic Bank (ADIB), is the world’s first Islamic digital proposition to specifically target Gen Z users. Cocreated in 2021 with the Founders Club—a group of Emirati young people and their parents aiming to educate and empower young customers. Customers can receive allowances, send money to friends and family, create saving goals, and access a wide range of financial tools. Parental controls include monitoring and spending limits.

Money Diary

Launched in October 2021, Money Diary is the first teenager financial learning service in Taiwan that links parents’ accounts with their children’s. Money Diary was developed by CTBC to help Gen Z mobile natives gain financial literacy, while helping their parents manage their children’s financial status. Money Diary was created to suit teen tastes, needs and capabilities, with budgeting and savings gamified. Weekly reports of financial behavior are presented in shareable Instagram-like stories.

Dukhan mobile app enhancements

Dukhan Bank launched several mobile banking firsts in Qatar in 2021, such as integrating Apple Pay with a loyalty program (Dawards) and mobile-based stock trading and account management. Other services added to its mobile app in 2021 included cardless cash withdrawal, instant opening of foreign currency accounts, Shariah-compliant fixed deposit accounts and “Wadiati” term deposit accounts, and controls over card transactions and usage.

Weyay Bank

Weyay is Kuwait’s first digital bank, created from the ground up, which has allowed the National Bank of Kuwait (NBK) to work closely with a dynamic community of shabab (Kuwaiti youth) who helped cocreate Weyay’s unique journeys and services to suit the needs of Kuwait’s younger, digital-native generation. Weyay launched in November 2021. Customers 15 or older can open a Weyay account by digitally onboarding using their Kuwait mobile ID. Weyay also boasts fully digital account management and allowance transfer and plans to add new services this year, including rapid peer-to-peer payments, savings accounts and goals, bill-splitting, and integrated brand partnerships.

TD AI-powered personalization platform

TD Bank’s AI-powered personalization platform, rolled out to all mobile users in 2021, provides tailored actions and insights based on banking behavior, to help improve customers’ financial wellness. With eight patents pending, and proprietary advanced machine learning algorithms developed by a globally recognized leader in machine learning and predictive analytics, TD Bank has created a client-centric platform that uses AI-driven nudges to offer proactive insights that are personalized and contextual to the customer, such as low-balance prediction and upcoming transactions to alert the customer and to advise on possible actions.

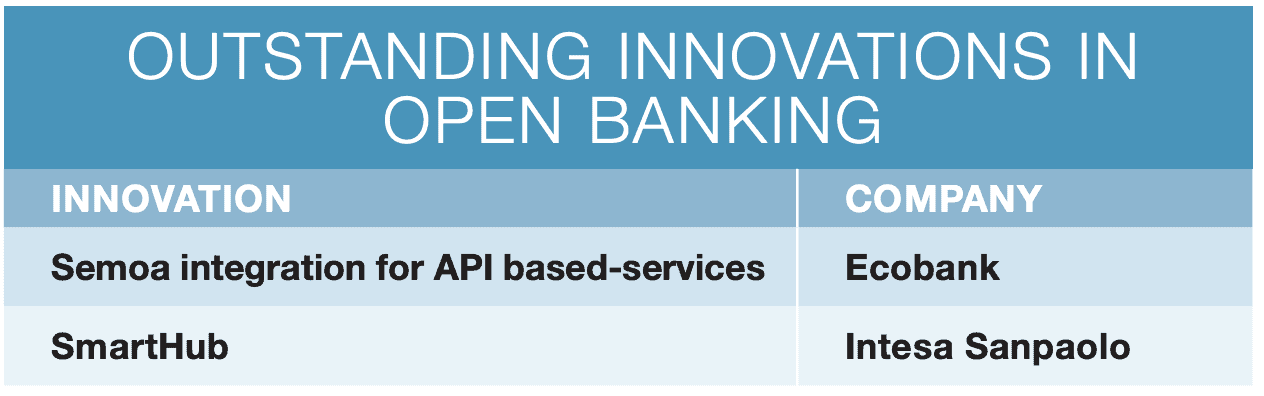

Semoa integration for API-based services

In July 2021, Ecobank was the first bank to extend its Xpress Cash e-token generating service to third parties via fintechs. Xpress Cash enables customers to send money without using their debit card. By partnering with Semoa—a fintech from Lomé—Ecobank is using open banking to enable mobile-money users in Togo to carry out banking across the West African Economic and Monetary Union, with a new digital-banking service via WhatsApp called Express Cash by Semoa. By allowing Semoa access to Ecobank’s infrastructure, people with no bank accounts or credit cards can cash out their mobile money directly from Ecobank ATMs and Xpress Points.

SmartHub

SmartHub, Intesa Sanpaolo Group’s open banking portal, is the first site in Italy that allows customers to access APIs, products and services offered by a bank. SmartHub was officially rolled out in December 2021 and provides a platform for corporate clients to integrate the bank’s functionalities in the most direct, efficient and secure manner. It also acts as a meeting hub between banks, companies and developers—providing a fertile platform for new business opportunities. Currently focused on corporates as well as SMEs, SmartHub includes products and services in collaboration with strategic partners.

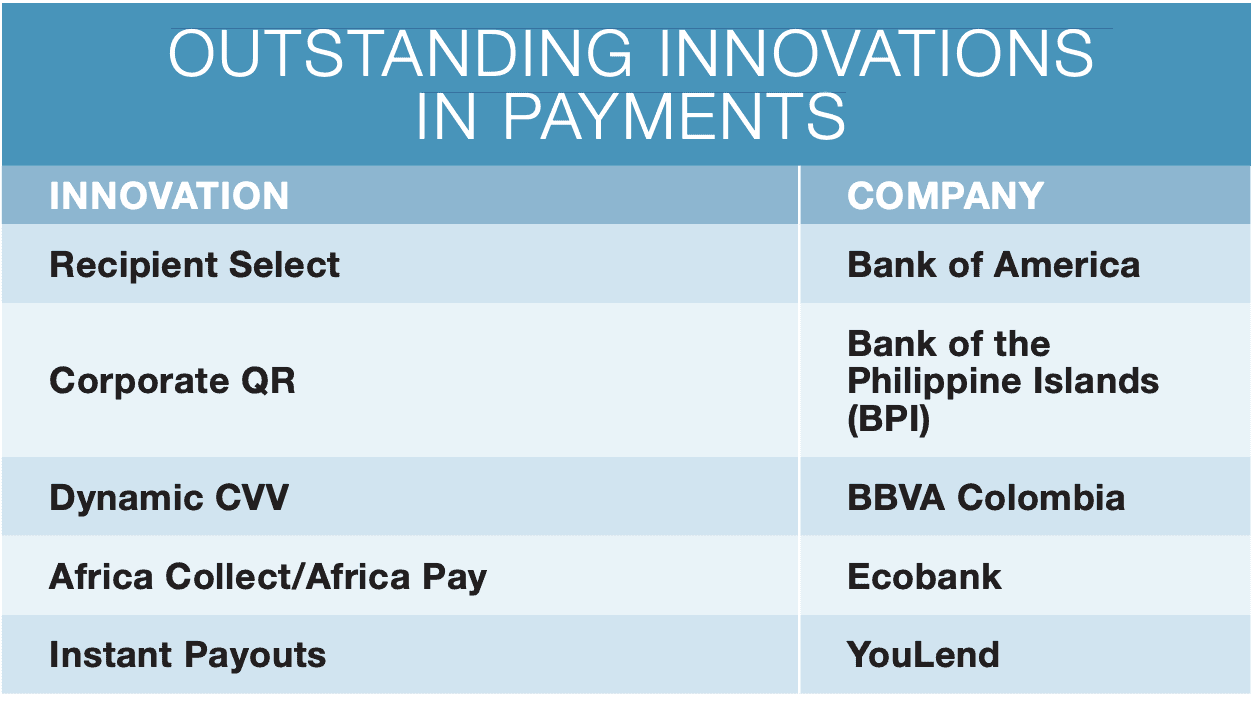

Recipient Select

Bank of America’s Recipient Select is the first business-to-consumer (B2C) digital payout platform that allows customers to choose their payment method. It features a broad range of payment options in the US: Zelle, PayPal, real-time payments, Automated Clearing House (ACH), check, and Pay to Card. And it has three global payout options: cross-border wire, cross-currency ACH, and PayPal. It improves digital uptake of payments and helps companies avoid collecting and storing payment information and reduces errors through upfront validation of data.

Corporate QR

Bank of the Philippine Islands (BPI) Corporate QR facility was launched in April 2021 to collect payments from businesses and corporate individuals in real time. Riding on the retail version of the QR code fund transfer facility for individuals, BPI saw the potential for companies to collect in the same manner. BPI says that QR codes are both quicker and faster for small businesses, as they negate the chance of inputting erroneous account details.

Dynamic CVV

BBVA Colombia is the first bank in the country to have dynamic CVV on debit cards to protect against fraud. A new dynamic code, requested via mobile or internet, is generated for every purchase. The decision to add dynamic, one-time purchase codes coincides with the rise in online shopping.

Africa Collect/Africa Pay

Launched in December 2021, Africa Collect/Africa Pay is the first pan-African solution that can centralize customer collections and payments. Ecobank collects instantly on behalf of its customers through various channels and across the 33 countries in which it operates. For merchants who are not incorporated in every country where they have operations, Africa Collect/Africa Pay is a streamlined solution providing more-accurate and timely information for collections, all via a single integration with the bank.

Instant payouts

YouLend went live in March 2021 with the first embedded provider-agnostic instant-payout solution to enable e-commerce platforms or payment service providers to reduce three-to-five-day payout times to just minutes. YouLend is delivered via a simple suite of APIs.

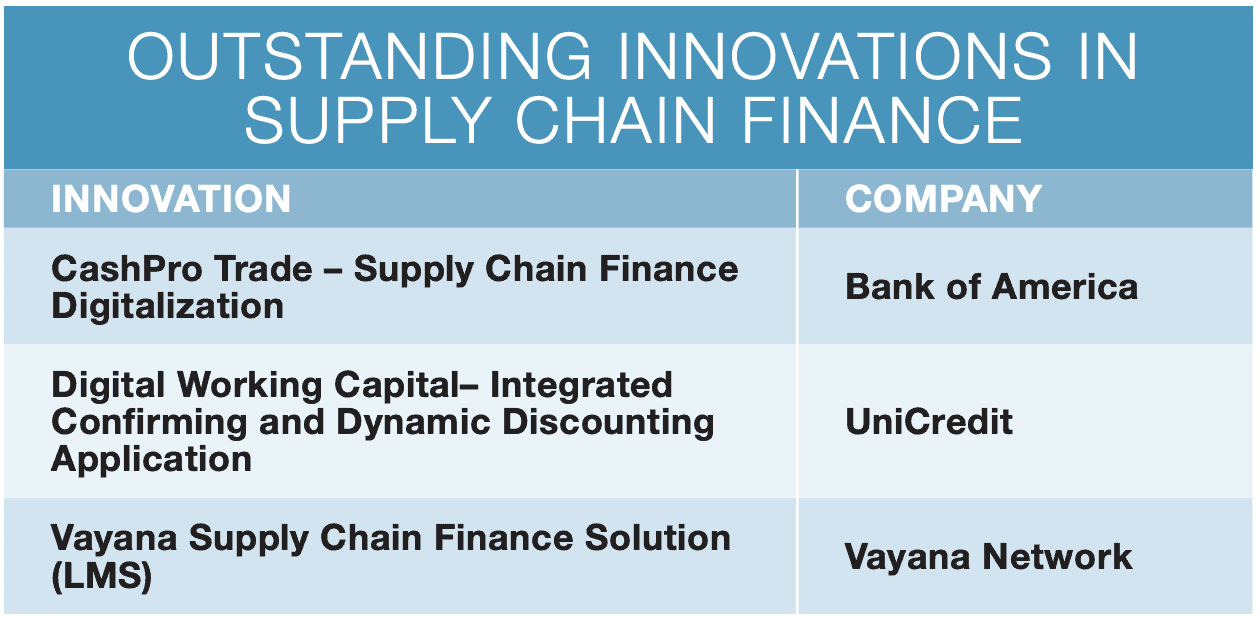

CashPro Trade

Bank of America says it is the first bank in North America to launch a third-party module that allows supply chain finance service providers to seamlessly connect to a portal—its CashPro Trade—for streamlined financing of approved invoices and digital status updates through APIs or file transmissions. The bank says third parties such as the Marco Polo Network, a trade consortium based on blockchain technology, can use the module to access the bank’s CashPro Trade portal. “This collaboration will expand our market offerings to suppliers of all sizes, providing smaller suppliers with more-favorable financing rates and buyers more stability in the supply chain,” says the bank.

Integrated confirming and dynamic discounting application

In Italy, UniCredit combined two different supplier-financing solutions—confirming and dynamic discounting—into one, with its digital working capital, integrated confirmation and dynamic discounting application. The fully digital application creates a single entry point for the two, which are usually sold as separate solutions.

Vayana SCF solution

Vayana Network calls its full-stack financing platform the first for banks and financial institutions in India: a solution designed to address some of the challenges—integrating multiple types of parties and company systems—faced by many banks in scaling up supply chain finance offerings. It is also geared toward making supplier financing more user-friendly for SMEs, allowing small businesses to access financing without having to engage in time-consuming, paper-based processes. The system also works in real time, which means every disbursement or repayment is reflected in limits measured in seconds. In earlier systems, Vayana says this process could take up to 30 minutes—a long time in SCF.

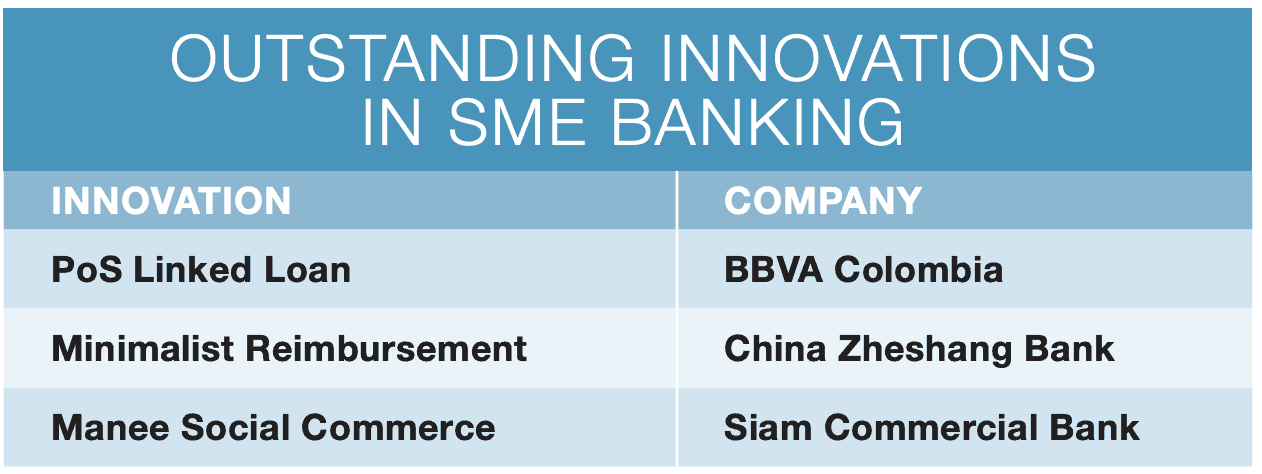

PoS-linked credit

BBVA Colombia wasn’t offering credit to many of its regular customers because they weren’t able to provide the necessary documentation, so it developed point-of-sale (PoS) linked loans, giving credit to SMEs and individuals who normally don’t obtain financing from the bank. BBVA reviews the small businesses’ monthly transactions and, using an adjusted risk analysis, advances funds. The SMEs give a promise to repay; they have two months to repay this advance. BBVA is the first bank to offer a loan SMEs can access with just one click.

Minimalist reimbursement

Traditional reimbursement models have cumbersome procedures and slow account receipts, restricting a company’s financial management. China Zheshang Bank developed a software-as-a-service-based expense-control system—Minimalist Reimbursement—that includes a unified process control, image management and capital payment. Companies can process invoices with one click. The platform has four major module functions: third-party service, reimbursement management, salary management, and connected data . This platform streamlines processes with third parties, for example, that provide travel, catering and other services by connecting the supplier and managing the process so employees do not have to use advances and invoices.

Manee Social Commerce

Social commerce is a growing trend in Thailand, but small businesses are challenged by the variety of platforms and channels. Siam Commercial Bank solved this problem with Manee Social Commerce, Thailand’s first seamless all-in-one merchant solution designed specifically to help entrepreneurs manage online stores with respect to inventory and order management, payments, fulfillment, digital lending and merchant engagement. Siam Commercial Bank also offers various payment options through Mae Manee Bill and courses for entrepreneurs through Manee Academy. Entrepreneurs earn loyalty points for each payment transaction through Manee Reward.

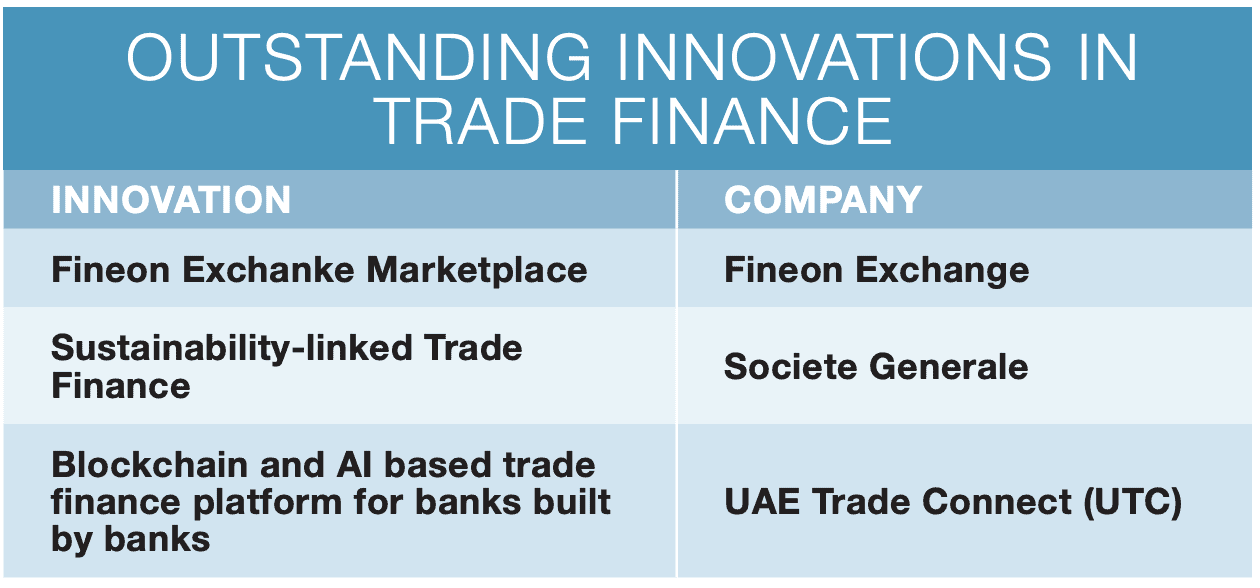

Fineon Exchange marketplace

To improve access to trade finance globally, especially for small businesses, Fineon Exchange developed the first trade finance marketplace to provide intermediaries with a full suite of transaction brokerage tools complemented by a digital interface with financial institutions. The marketplace uses an algorithm to quickly identify compatible partnerships for funders and companies seeking trade finance, and Fineon facilitates the data exchange between the parties. The algorithm considers the funder’s risk appetite regarding the sector, jurisdiction, asset type and volume, to ultimately increase transaction turnover. Corporates can use the marketplace to increase sales and optimize their working capital while minimizing risk.

Sustainability-linked trade finance

Societe Generale is the first French bank to offer sustainability-linked trade finance, which supports the transition of “dirty” industries. Clients select specific environmental and social objectives and Societe Generale grants a bonus on fees if the goals are met. ESG key performance indicators may include reducing greenhouse gas emissions by a certain amount, training a percentage of employees to prevent fraud or corruption, or reducing greenhouse emissions by a specified amount. Societe Generale relies on audit or report certificates to confirm whether goals are achieved.

Blockchain/AI-based trade finance platform for banks

UAE Trade Connect (UTC), with Etisalat, developed the first national trade finance blockchain platform for banks in the UAE, taking the risk out of trade finance in the banking sector. UTC is a consortium of seven banks: First Abu Dhabi Bank, Mashreq, Emirates NBD, Commercial Bank of Dubai, Commercial Bank International, RAK Bank and National Bank of Fujairah. The banks provided domain knowledge and Etisalat Digital developed the solution and provided the cloud infrastructure. With this platform, parties can exchange data on the distributed ledger without being exposed. The platform’s AI and machine learning engines identify duplicate invoices and fraudulent activity.

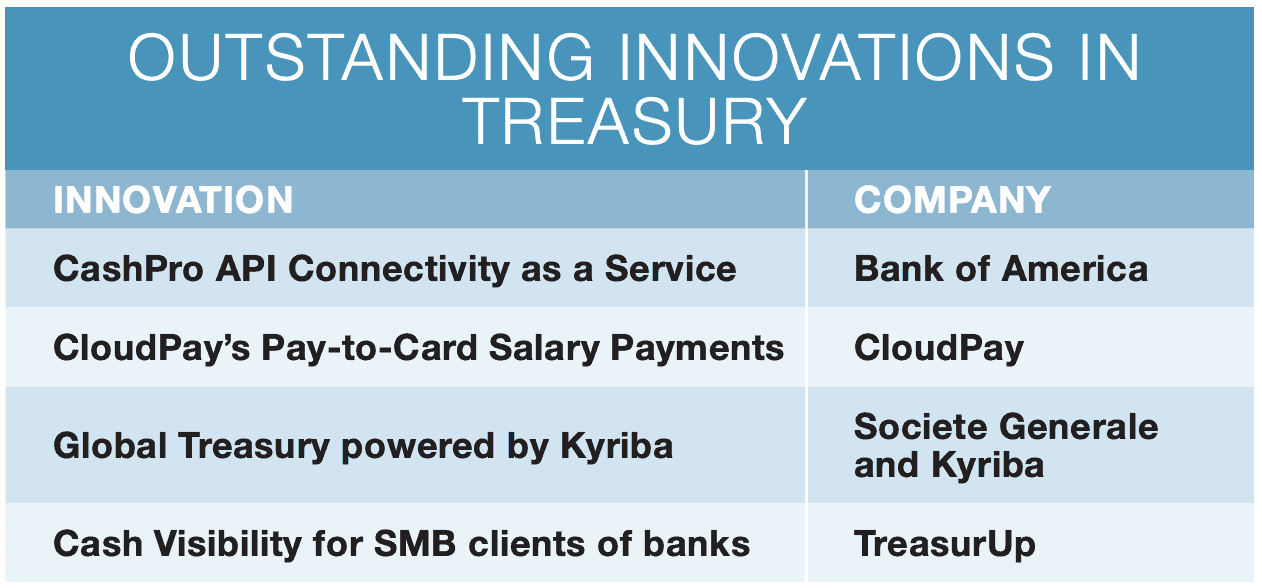

CashPro API connectivity as a service

As the first financial institution to openly collaborate with a fintech to combine APIs and file-transmission connectivity to accelerate onboarding of a payment initiator, Bank of America (BofA) can reduce a client’s onboarding from an average of eight weeks to roughly 10 hours. By standardizing the connectivity paths with the most popular ERP systems, BofA can accelerate access to the CashPro payment service. By offering CashPro API’s connectivity as a service, furthermore, the bank can generate API keys that enable data transfers from those ERP systems to ensure that all required data elements are present in those transfers for successful payment processing.

Pay-to-card salary payments

Launched in Oct 2021, CloudPay’s pay-to-card salary payments make paying employees via a direct deposit to their debit or credit card simple and compliant. By using a card rails network, once payments are set up and validated, money can be deposited into an employee’s account virtually anywhere in the world in as little as 30 seconds. Payments are no longer tied to fixed monthly payroll dates. It creates flexibility in how and when employees are paid and frees up payroll staff by drastically reducing the time needed to set up payees and run payment cycles.

Global Treasury powered by Kyriba

Built on the expertise of Kyriba, in November 2021 Societe Generale launched Global Treasury, a new scalable treasury management system and payments solution. With real-time monitoring of treasury positions and provisional management of liquidity flows, payment automation, banking delegation and mandate management, enhanced fraud management, multibank connectivity, ERP, payment validation, workflow management and more, Societe Generale aims “to simplify the daily treasury management of companies by targeting their essential needs in terms of payments, treasury and fraud management.”

Cash visibility for SME bank clients

Released by TreasurUp in the fourth quarter of 2021, this is the first open banking cash visibility tool banks can offer to their SME clients that is fully integrated with FX hedging and FX cash flow forecasting. This treasury management system module, or “light TMS,” is solely developed and white labeled for banks to offer commercial banking clients. TreasurUp’s cash visibility module is based on the latest open banking (Payment Service Providers Directive 2) standards and includes ERP integration. The journeys are integrated with its existing FX hedging module.

App Popular’s digital claims

Banco Popular launched the Dominican Republic’s first mobile digital claims solution for banking clients, and one of the first such applications for Latin America. Instead of having to visit a bank branch, customers using the bank’s mobile app can now formalize a claim in a few minutes. Better still, regardless of where the claim was first lodged (online or in a branch), the app also allows customers to track their claim’s status—no more waiting on the telephone to see what is happening. The bank says its digital solution formalizes claims in less than five clicks. And if customers are not happy with a claim’s status, they can interact with claims departments using the same app. No more disconnects between the online and offline World’s.

Plink

Banistmo Bank’s Plink analytical tool—the first nonfinancial product in Panama under a B2C platform—uses transactional data and analytics to help business leaders gauge the health of their businesses. The tool conducts statistical analysis of consumption habits and more to help businesses find customers, measure high and low sales days, and identify most profitable prospects for new outlets. Customers can view transactional information on a user-friendly dashboard, and heat maps enable businesses to easily pinpoint trends.

Redesigned UX

In July 2021, Citibanamex launched a redesign of its home page—the first, it says, to prioritize the user experience (UX) through a modular design with dynamic components to help customers more easily access information pertaining to financial products, help tools and education. “We wanted citibanamex.com not only to be a communication channel, but also to be one that considers the main needs and problems of our users in a dynamic and empathetic way,” the bank states. “We wanted our users to have a marketplace and self-service together.” The 100% mobile browsing experience helped reduce the site’s bounce rate, and citibanamex.com now ranks No. 1 in Mexico for financial planning and management.

Financial wellbeing platform

The UX of all UX must be Dreams Technology’s financial well-being platform (FWP) for the business-to-business market, launched in May last year. Taking inspiration from fitness apps, the platform purports to be the first FWP that applies psychology, neuroscience and behavioral economics to “nurture deep engagement” between customers—largely Gen Zers, millennials and women—and their finances. Think of it as personal financial management on steroids, something long talked about that few companies have been able to achieve. Even then, Dreams admits it took almost a decade’s worth of R&D and collaboration with experts from Harvard, UCLA and University of Toronto, to get its solution, currently available only in Norway and Sweden, to where it is today.