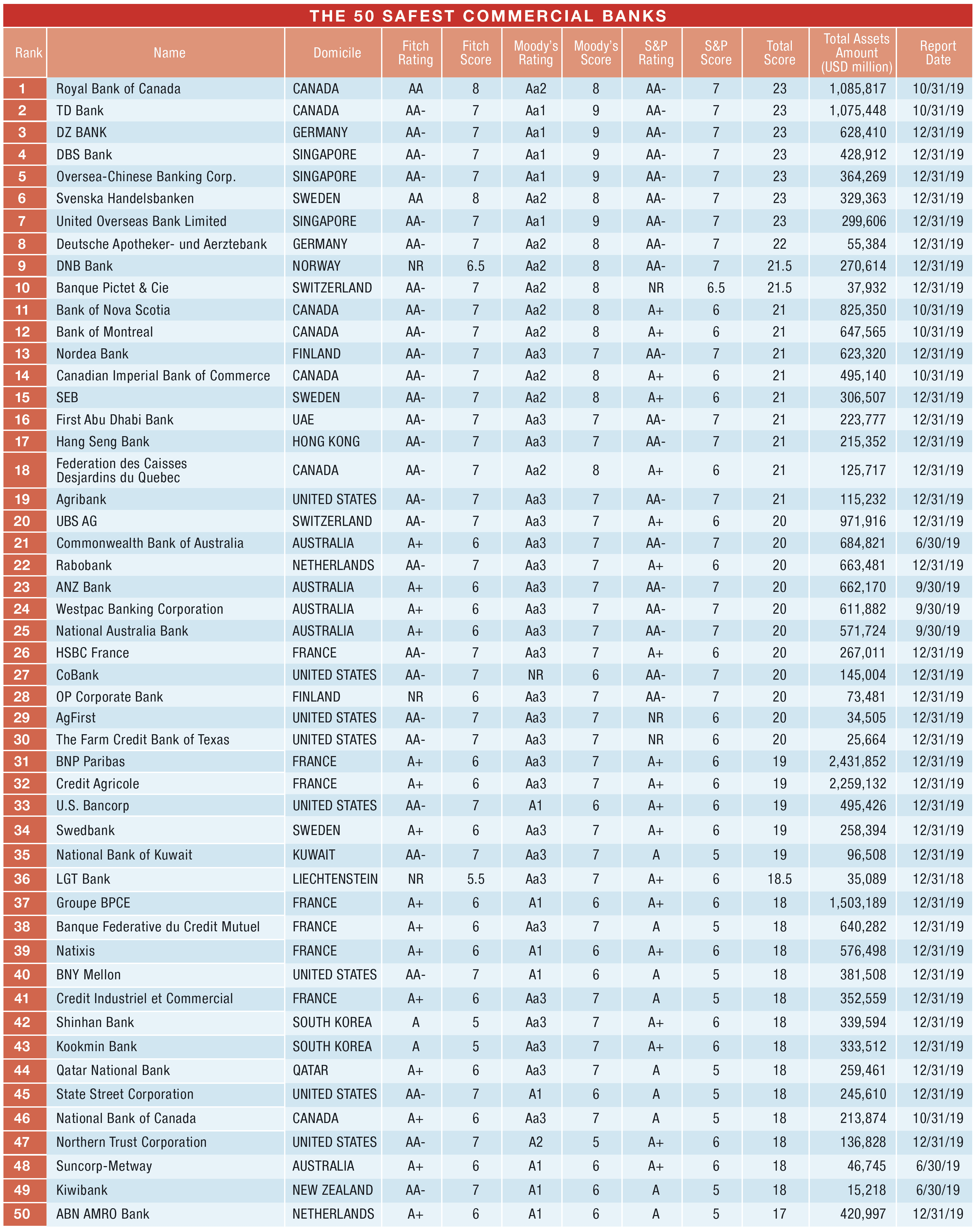

Global Finance names this year’s 50 safest commercial banks.

Commercial banks have been focusing for years on the transformation of their business models to leverage digital technology, but the Covid-19 pandemic has accelerated this process. Executives recognize the need for greater operational efficiency as customer expectations increase beyond mobile applications and online-payment capabilities. As their customers isolate, and as they, in many cases, switch their employees to working from home, they need to adopt technology advancements to better enable them to target clients and markets.

The pandemic and resulting pressures on the sector produced some significant shifts in this year’s Safest Commercial Banks rankings. Four Australian banks: ANZ Banking Group, Commonwealth Bank of Australia, National Australia Bank and Westpac sustained downgrades to A+ from AA- from Fitch Ratings on concerns about bank profitability and asset quality.

Many of the institutions that earned a spot in Global Finance’s ranking of the Safest Commercial Banks exhibit strong capital ratios, and a solid funding and liquidity profile will help them endure potentially sustained declines in profitability. All feel the pain of the economic contraction precipitated by the pandemic; however, it remains to be seen which ones emerge stronger. With top-line revenue growth proving elusive, commercial banks are in close competition to differentiate themselves and gain an edge in operational efficiency. The pace of technology spending continues to pick up.

A New Era

Recent years have seen a marked rise in new rules for bankers around money-laundering and other ethical and legal questions. This year, Swedbank fell sharply, to No. 34 in the ranking, as the discovery of deficiencies in its compliance with AML laws prompted all three agencies to downgrade it. HSBC France and National Bank of Kuwait both also moved down following downgrades—by Standard & Poor’s.

In a new era of banking, both consumers and corporate clients are benefiting as mobile banking applications and lending platforms give them quicker and easier access to credit. While the largest and most diversified banks continue to refine their current offerings, they are rushing to develop additional capabilities that better utilize data analytics.

Artificial intelligence (AI) is critical to the more complex types of data analysis banks demand and is at the heart of the sector’s technological transformation. AI allows commercial banks to efficiently explore data for new product development, client acquisition and retention, risk management, fraud protection, cybersecurity and anti-money laundering (AML) compliance and detection. Case in point is this year’s top-ranked commercial bank, Royal Bank of Canada, whose Borealis AI research division rolled out to clients an AI-based electronic trading platform using an algorithm that promises to improve equity trade execution.

In a positive development for payments, the European Commission (EC) adopted a Retail Payments Strategy in September, which the EC said is intended to reduce market fragmentation, “creating the conditions that make it possible to develop instant payments and EU-wide payment solutions that are cost effective and accessible to individuals and businesses across Europe.” With change, new entities rise to the ranks of the safest. Natixis and Credit Industriel et Commercial are new entrants this year.

The commercial banking sector is experiencing profitability pressure, margin compression and rising credit costs as its loan book deteriorates in vulnerable sectors. New exposures will require an upfront reserve for loan-loss expenses, as directed by the Financial Accounting Standards Board’s current expected credit loss model and the International Financial Reporting Standards IFRS 9 accounting treatment, rather than an estimate of incurred loss at the time a loan is originated.

Commercial banks that are majority state owned or receive sponsorship by their governments or regional bodies are excluded from the Global Finance ranking. Institutions included here may operate in the same markets as state-sponsored competitors but don’t benefit from government backing.