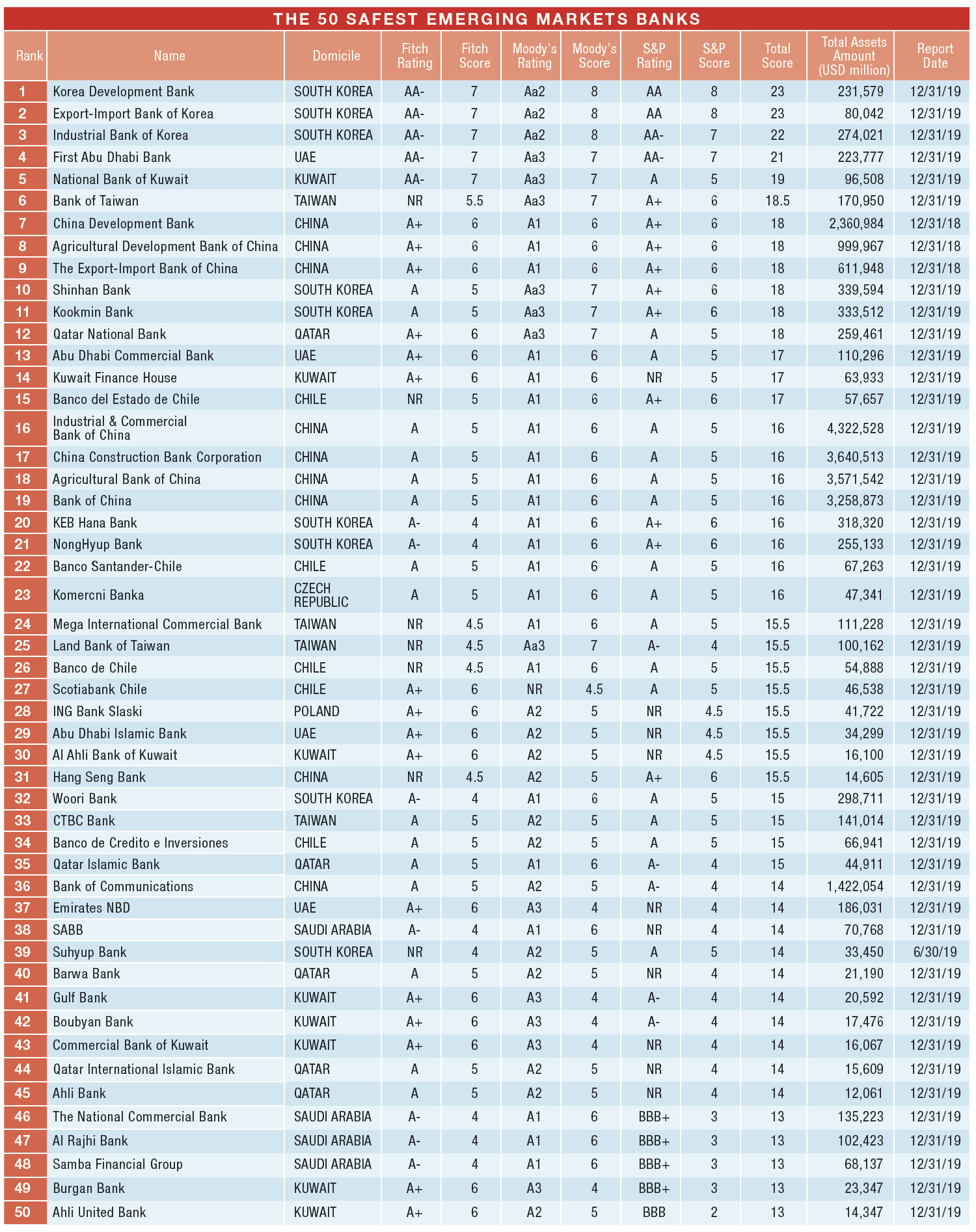

Global Finance names this year’s safest banks in emerging markets.

With emerging markets facing the twin ills of the coronavirus pandemic and rising debt loads, banks and other financial insituttions have been critical sources of strength and stability. Since the start of the outbreak, emerging market countries have been contending with severely weakened economies, high unemployment, rising business failures and social and political unrest. The International Monetary Fund (IMF) World Economic Outlook October update predicts a 3.3% GDP contraction for these nations in 2020, followed by 6% growth in 2021—only slightly better than its global forecast of a 4.4% decline this year and a recovery of 5.2% next year. If China—the only major economy for which the IMF predicts positive growth for 2020—is excluded, the emerging market forecast worsens.

Against this backdrop, a ratings upgrade is indeed good news, and the biggest mover in this year’s ranking of the World’s Safest Emerging Market Banks was Poland’s ING Bank Slaski, which gained 12 places from its 2019 ranking. Fitch upgraded the bank in April, citing greater loss-absorbing capacity from junior debt buffers raised by its parent, ING Bank.

With banks that receive the same score ranked according to asset size, mergers and acquisitions can have a big impact, too.

Barwa Bank, which strengthened its position in the Qatar banking system with its 2019 merger with International Bank of Qatar. The increase in assets as of year-end allowed Barwa to move up in rank by 6 spots under our methodology.

Strengthening Defenses

Emerging market banks are grappling with the economic fallout from weaker global trade flows, interruptions in international supply chains and volatile commodities markets, all of which are wreaking damage on their domestic industries. The IMF forecasts a 10.4% decline in world trade volume this year. Significant weakness in the oil market will produce a 32.1% decline in oil prices this year, the agency predicts, hitting oil-exporting countries hard. All of these pressures spell eroding asset quality for banks based in these markets.

As conditions worsen, emerging markets are also at risk of capital outflows from declining foreign direct investment, a retreat by investors in equity and fixed income portfolios, and potentially greater difficulty issuing debt in disrupted markets. Emerging market nations are sensitive to foreign currency fluctuations. Since March, a falling dollar has brought some relief by way of cheaper imports and declining service costs on US dollar debt; but conversely, emerging market countries’ exports are now relatively more expensive. In response to currency strains, some countries are opening bilateral swap lines with the US Federal Reserve Bank for their central banks and other major banking institutions to help service US dollar-denominated debt.

To help alleviate the considerable stress, central banks in many emerging markets have responded with interest rate cuts, direct stimulus for health care and unemployment benefits and increased systemwide liquidity through asset purchase programs, loan guarantees and forbearance. The IMF and World Bank have pledged $1.2 trillion in aid to help emerging economies. The IMF and Unctad said that developing countries have an immediate need for $2.5 trillion in aid.

Rating agencies have conveyed an increasingly negative ratings bias to many emerging market banks, prompted by the weakening operating environment and the worsening state of their assets. Recognizing that loan forbearance and debt moratoriums would only delay bad-debt recognition into 2021, Standard & Poor’s expects nonperforming loans to rise by 50% on average—doubling in some countries as the agency lowers its expectations for the most vulnerable sectors. Any sovereign downgrade, moreover, would likely prompt follow-on downgrades of the country’s largest banks, given that they derive a boost from the expectation of sovereign support embedded in their ratings.