U.S. lawmakers are upset with China. Again.

The most recent object of their ire is the aluminum sector, which has amassed considerable overcapacity in the face of falling global demand. In October, eight senators asked the Obama administration to take action against China alleging unfair subsidies to the Chinese Aluminum industry.

In fact, last year China’s aluminum industry received RMB 2.7 billion in government subsidies. To contextualize that number, you should know that those same aluminum producers went on to lose RMB 1.5 billion. Chalco, the largest aluminum producer in China, pulled down nearly RMB 830 million of “Enterprise Development Support Subsidies” as revenues fell for the third straight year. So, you can see why the senators are upset.

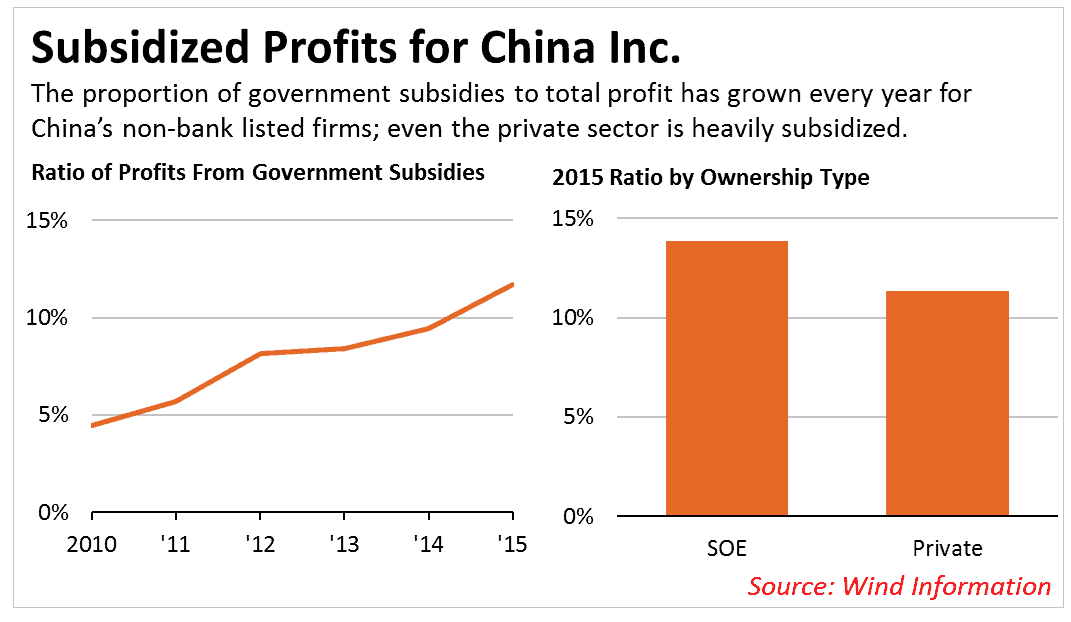

But it’s not just the aluminum industry; subsidies comprise a growing fraction of profits for Chinese firms in all sectors. For example, from 2010 until 2015 the ratio of government subsidies to net profit for non-bank listed firms tripled to 12%. While one might expect the bulk of that to be going to China’s state-owned-enterprises, even the private sector attributed 11% of last year’s net profit to subsidies.

Given the growing government support of Chinese listed firms, many of which compete for market share internationally, it is important to understand who is benefitting and how much.

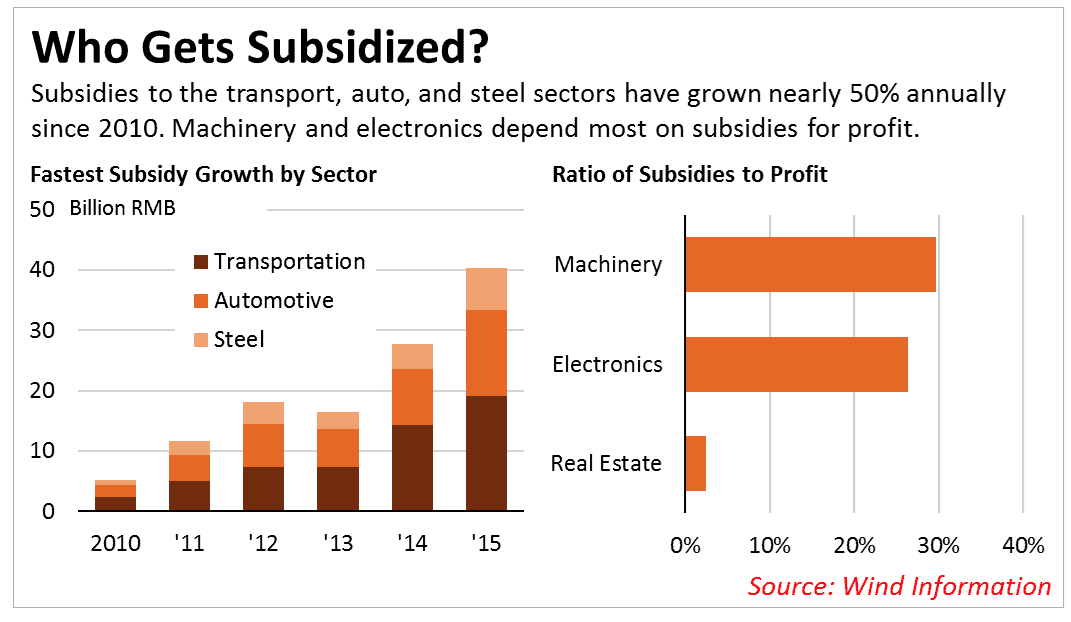

Since 2010, the first year we have comprehensive data, government subsidies have grown the fastest for the auto, transport, and steel sectors. The industries that depend most on subsidies are the building machinery and electronics sectors. China’s frothy real estate sector, which neither hurts for funds nor books significant revenue from overseas, received the least government subsidies as a percentage of profits.

The Chinese government grants subsidies to enterprises for two main reasons.

First, the government leans on enterprise – both state-owned and private – to tackle development goals. The government will grant debt forgiveness, tax rebates, or cash to firms that have promising projects or are responsible for high levels of employment. Additionally, China’s leadership is determined to build a legion of internationally competitive enterprises, an initiative which they support extensively.

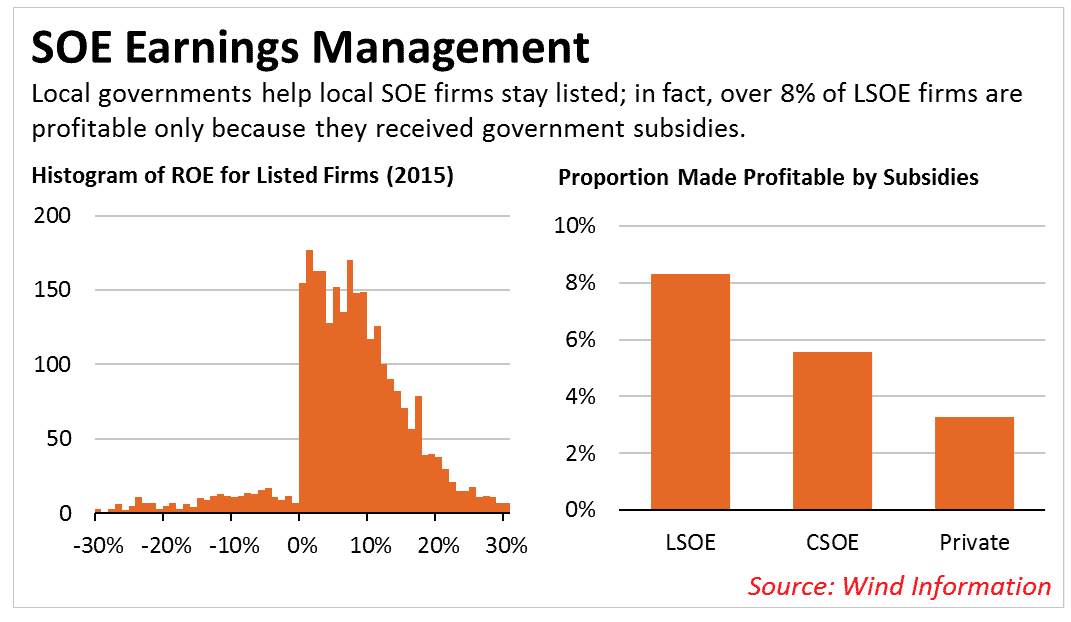

Second, local governments grant subsidies to help SOEs clear regulatory hurdles. China’s securities regulator imposes penalties on firms that post consecutive years of losses; so, earnings management is rampant as firms use every trick at their disposal to avoid consecutive loss-making years. This unique regulatory environment creates novel incentives for SOE firms and the local governments that support them.

In fact, over 8% of listed local SOEs are profitable only after receiving subsidies – that is, they would have recorded a net profit loss without a helping hand from the local government – which more than doubles the mark for the private sector.

For years, the Chinese government supported SOEs and favored private sector firms with cheap bank loans to compete internationally. As profitability in home markets has deteriorated, the government added direct cash subsidies to its toolbox as well. Subsidies continue to be a point of contention in global trade discussions, and it remains to be seen how EU and US maneuverings—legislative or judicial—might impact Chinese policy.