With growth slowing, Beijing pushes technology, innovation and urban experimentation as the keys to China’s future economic ascendancy.

Smartphone giant Xiaomi recently stepped far beyond its comfort zone and into the latest phase of China’s economic development with a new domestic real estate venture. Last fall’s surprise announcement that 2,000 housing units would be developed by a property division of Xiaomi, best known for affordable smartphones, highlights the changes rippling through the Chinese economy amid slowing growth and volatile trade relations with the US.

Xiaomi is one of numerous Chinese companies now pursuing business innovation while heeding Beijing’s call to boost support for the “real economy”—i.e., Main Street—even if it means blurring the lines between traditional sectors such as electronics and real estate. Another innovator is Geely Group, a domestic vehicle manufacturer and owner of Sweden’s Volvo Cars. Geely recently launched a luxury ride-hailing venture in China with Germany’s Daimler. The move fits what Geely Technology Group CEO Liu Jin Liang describes as Geely’s “continued transformation as a mobility and transport technology company.”

An appetite for innovation has helped fuel China’s ascent to economic prominence over the past 40 years. Today, Beijing hopes it will offset external factors weighing on the world’s second-largest economy. Innovation also underpins China’s ongoing urbanization and shift from basic manufacturing to robotics, smart cities, electric vehicles and artificial intelligence (AI). “China has a long tradition of experimentation and adaptation,” Andrew Sheng, a distinguished fellow at the University of Hong Kong’s Asia Global Institute, and Xiao Geng, president of the Hong Kong Institution for International Finance, in a recent commentary.

Business innovation is also about survival. Shortly after the US Census Bureau reported that the US-China trade deficit in goods fell a staggering 30% last November year-on-year, Chinese policymakers at the annual Central Economic Work Conference acknowledged that “the country faces rising downward economic pressure.” They pledged to encourage “structural adjustments” in 2020 through state enterprise reform and emphasize the role of science and technology as growth drivers.

Consider AI, a sector China aims to dominate globally, and its financial-sector applications. Business is booming for companies like Pintec, a Nasdaq-listed fintech that digitally links financial institutions such as banks and securities firms with businesses like online travel agents and telecoms. Pintec recently announced a tie-up with the 320-million-subscriber China Unicom that lets online customers lease-to-own smartphones with no down payment.

Giants of digital transactions and consumer financing have emerged in recent years from humble beginnings on the e-commerce platform Alibaba and social media’s Tencent. Alibaba’s Alipay and Tencent’s WeChat Pay are now mainstays for quick, cashless smartphone payments for everything from McDonald’s hamburgers to traffic fines.

In its fiscal third-quarter report, Hong Kong-listed Tencent said monthly users of its WeChat messaging app, the umbrella for WeChat Pay, had soared to 1.15 billion, up 6.3% year-on-year, and its business services revenues rose 36%, to $3.9 billion, thanks in part to “increased daily active consumers and number of transactions per user.”

That’s not to say China’s innovations are entirely homegrown. Piero Scaruffi, a Silicon Valley author and technology pundit who frequently speaks at tech conferences in China, notes that for years, Chinese businesses have found ways to profit from other countries’ scientific research. “It was a smart strategy,” he says. “The United States, Europe, Israel, Japan, South Korea, etc., took all the risk while China waited. Whatever worked, China applied.”

China is, he adds, “very good at applying new technology on a very large scale. Using a phone to pay is still rare in the US, whereas it has been common in China for years.”

Now China’s mobile-internet system is being quickly upgraded to 5G speed—albeit limited by government censorship. The upgrade was formally rolled out for consumers last fall by the three state-owned telecoms. The switch to 5G is also being promoted by smartphone and equipment makers such as Huawei Technologies, which is marketing the innovation abroad and at home.

While China’s 5G push faces opposition from other governments, notably Washington, the ambition is impressive. “The ubiquity of mobile devices and cellular capacity and density is without equal, and 5G deployments in China are expected to reach 1 billion devices by 2025,” says Joe Weinman, an author and former AT&T executive who specializes in cloud computing.

“China has proven itself capable of major technological breakthroughs in information and communication technologies, and other segments,” he adds. Moreover, China “has the cultural, financial, governmental and human elements that are essential to move technologies from ideas to successful commercialization and widespread adoption.”

The economy will need more than fast internet to reach the government’s declared target of around a 6% GDP growth rate in 2020, compared to last year’s rate of 6.1%. The World Bank has predicted a cooling to 5.9% this year.

For that reason, innovation is the watchword for infrastructure and real estate development as well, including an initiative to create city “clusters” through interurban transportation, commercial and residential networks. The current buildout affects Hong Kong and nine mainland cities in the Pearl River Delta region; a northern region centered on Beijing and Tianjin; and the Yangtze River Delta area, including Shanghai. The government expects these three urban clusters to spur competition among businesses and “serve as platforms for further experimentation,” Sheng says.

Urbanization, in turn, feeds the real estate industry, which has been a major wealth generator for companies and individual investors alike since the 1990s. Long before Xiaomi got involved, local governments were raising funds by selling land to developers that then sold commercial space to businesses and apartments to families. Many Chinese consider property a fail-safe investment.

Property investment boomed last year. China’s National Bureau of Statistics clocked year-on-year growth in property development investment at 10.3% between January and October, totaling some $1.6 trillion. Residential investment alone rose 14.6%.

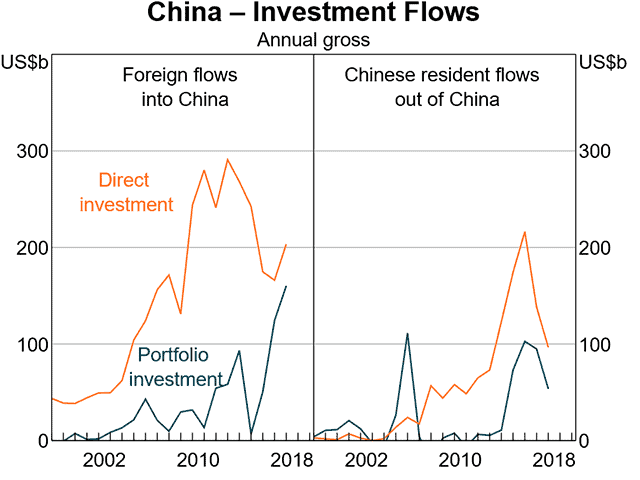

More foreign investors, too, are playing the Shanghai Stock Exchange, despite the slippage in GDP growth and exports to the US. A December report by China Merchants Securities predicted 2020 would see net inflows of foreign investment to mainland stocks, thanks to a stable renminbi-dollar exchange rate and an expected easing of US-China trade friction. The Reserve Bank of Australia Bulletin reported in September that foreign investment in Chinese stocks and bonds has been rising fast and could reach $405 billion in new portfolio inflows over the next three years. Meanwhile, inflows from Chinese investors are falling.

Beijing is also improving its institutional platform for innovation by, for example, acquiring successful Western companies and urging Chinese scientists working abroad to come home. China is “building or acquiring all the elements necessary to drive the often-unpredictable evolution of innovation,” Weinman says: “leading universities, scientists, high-tech firms, entrepreneurs, early-stage funding from both the private sector and various levels of government.”

How well the strategy works remains to be seen. “China is getting serious about doing real research,” Scaruffi says, “but it won’t be easy to change the mind-set of university professors, students or startup founders to create a culture of real innovation. For three decades, they defined ‘innovation’ as applying what the West invented. Very often they made it even better. But changing that definition will not be trivial.”

Nevertheless, China clearly believes its future lies in pursuing new means of stimulating the economy through unique business ventures, innovative digital technology and urbanization. While the economy is slowing, growth continues.