Nigeria faces leadership, institutional and security challenges to building a sustainable economy. But first, it must break out of its second recession in four years.

Chronic instability has been the curse of Nigeria’s economy. Despite its huge oil and gas resources—or perhaps because of them—Africa’s biggest economy has been unable to prevent wide swings in its fortunes. This year, it slipped into a recession for the second time in four years. If Africa is to break the pattern, the country’s leadership must start implementing policies that for decades it has professed to follow without real commitment.

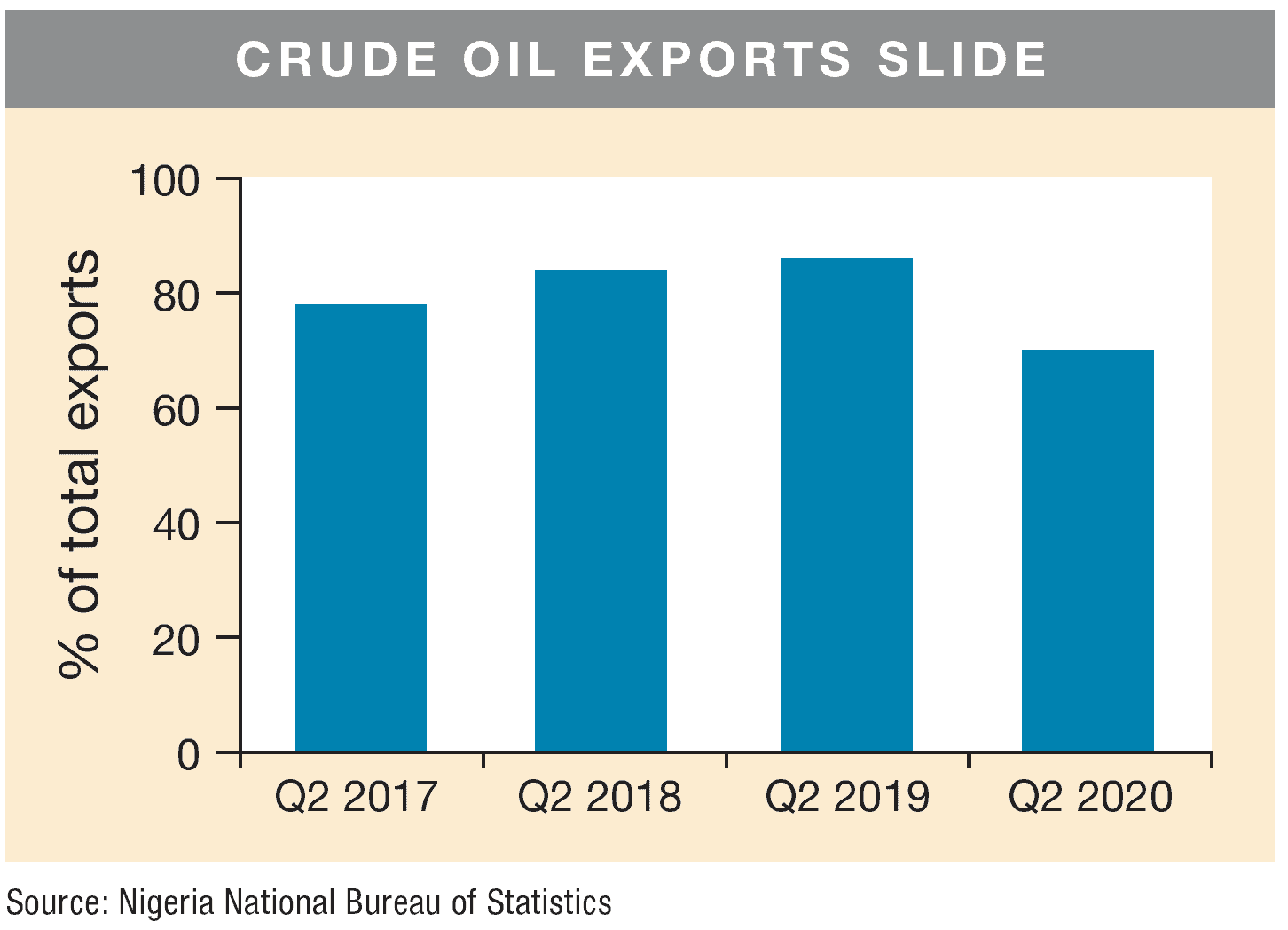

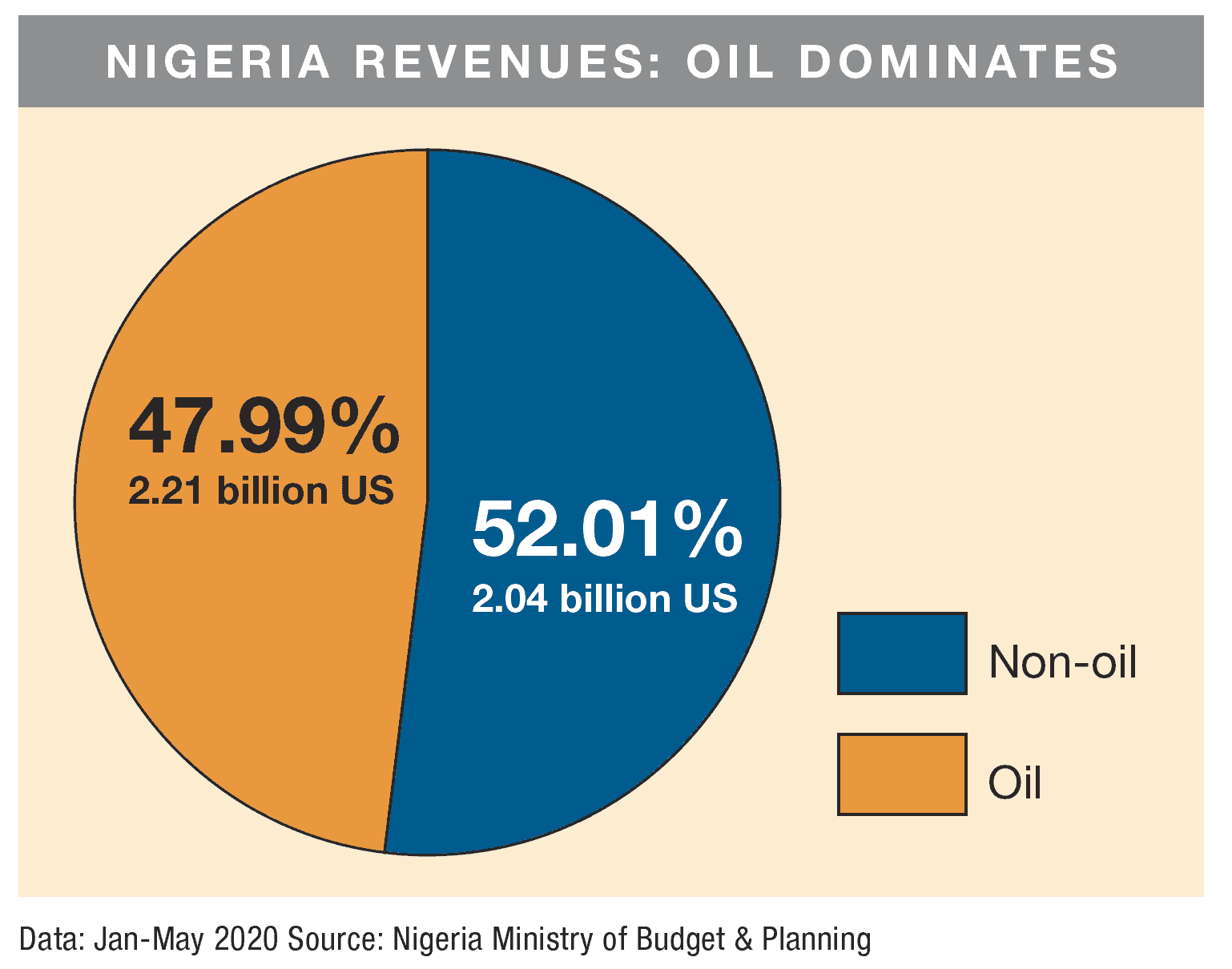

The economy fell 6.1% in the second quarter after posting a 1.9% growth rate in the first; in an October 7 budget presentation, Nigeria’s President Muhammadu Buhari projected another decline in the third quarter. But while the government has blamed the recession on the Covid-19 pandemic, which hit the country especially hard due to its near-total dependence on crude oil exports, analysts say the virus only exposed structural weaknesses in the economy.

Says Oghenefejiro Eduviere, Lagos-based foreign exchange (FX) trading associate at AZA, Africa’s largest nonbank currency broker, “The three things we must see in order for Nigeria to truly develop are diversification of the economy from crude oil, free float of the naira to attract foreign direct investment, and the development of enduring institutions and infrastructure to help weather challenging times.”

All three goals are still a considerable way off. Since the 1970s, when oil first became a significant item on Nigeria’s export table, petrodollars have flowed from oil exports while successive administrations allowed agriculture—formerly the nation’s top FX earner—to take a back seat. One consequence of Covid-19 has been a crash in the price of oil, notes Lagos-based economic consultant Marcel Okeke, as demand followed the collapse of business globally.

This knocked Nigeria’s 2020 budget out of balance. Budget estimates previously based on a benchmark oil price of $57 a barrel of oil and an official exchange rate of 305 naira per dollar had to be abandoned as the oil price fell as low as $20, the futures price dropped as low as $1 and the naira’s value plummeted to about 380 naira to the dollar—and around 460 naira on the black market.

“We have not really built a sustainable economy, because of the monoproduct culture,” says Okeke. “Incidentally, what we have been getting from oil has not been properly utilized.”

Leadership and institutional defects have plagued Nigeria since it attained independence 60 years ago, says Bongo Adi, Senior Lecturer in Economics at Pan-Atlantic University’s Lagos Business School, making the economy’s structural weaknesses that much harder to address.

“It is not a question of which sector should we start with,” says Adi. “It is still human beings. Before we get things going, we have to get the right cream of leadership in place; otherwise, we will keep on recycling, because Nigerians are not lacking skills or creativity.”

While Nigerian citizens have broken through to leadership and professional success in Canada, the UK, the US, Germany and other countries, Nigeria has been unlucky with leadership at various levels, Adi notes. He blames this on a “mendacious political system” built on the culture of imposition. This impedes the sustainability of good leadership and policies.

Law enforcement is the first institution that must be reformed for change to take root. “What is lacking in Nigeria is law and order,” Adi says. “Anybody can get away with anything because of the compromised police. Just get the right people into the police, and the system will autocorrect in less than a year. These are the guys who protect democracy, protect the state and protect the economy.”

Diversification and How to Achieve It

Nigeria recognized diversification as the solution to its vulnerability to the vagaries of oil; it’s been state policy for some time. But there has seldom been enough impetus to make it work.

Diversification has been couched generally as the production of everything non-oil for export: from agricultural products, to solid minerals to crafts and clothes.

The Central Bank of Nigeria (CBN), under its development finance program, has churned out funding schemes aimed at spurring activity in agriculture to raise output. The prime scheme is the Anchor Borrowers Program (ABP), which was launched in 2015. It links rural farmers to anchor companies contractually obligated by off-take agreements to buy the farmers’ output, thus ensuring sustainability. ABP also makes loans available to farmers at single-digit interest rates through money-deposit banks. The goal of ABP is to increase production of goods including rice, maize, wheat, cassava, cocoa, cotton and oil.

The problem, says Adi, is that the program aims to make Nigeria a producer and exporter of everything, rather than fashioning a complex export base. Instead of following the example of China, which tries to export everything, he argues, Nigeria should model itself after Vietnam, which Adi says has established itself as an exporter of “small things.”

“If you open your shirt, you could see that the button is made in Vietnam,” says Adi. “Look at your computer and you see that some of its components are made in Vietnam: not the whole thing, but they have a component.”

With such a targeted approach, Nigeria has a better chance to establish a competitive advantage, he contends. For a Chinese company that makes computers, for example, Nigeria can supply the keyboard, memory chip or screen; for a Japanese auto company, it can provide tires.

“I believe that we have the capacity to do such things using our natural endowment,” says Adi. “We have hydrocarbons that we have not maximized the use of. We have not gone into plastics. These are low-hanging fruits that government policies can unlock.”

The same value-added approach could be applied to all sectors of the economy, Okeke says. Nigeria should “get serious” with gas production, reducing its reliance on crude oil. First, it could shift to gas for domestic and industrial use; second, start refining crude oil locally and end its dependence on imported refined products. Currently, there are four state-run refineries, with a total capacity of over 445,000 barrels per day.

“Part of the impediment to the diversification agenda stems from the lack of proper infrastructure to support industrialization and growth,” says Janet Ogunkoya, Senior Research Analyst at Tellimer Research in Lagos. “Nigeria still battles with basic infrastructure issues such as adequate power supply and proper road networks. Also, many businesses still lack access to proper financing to engage in large-scale industrialization.”

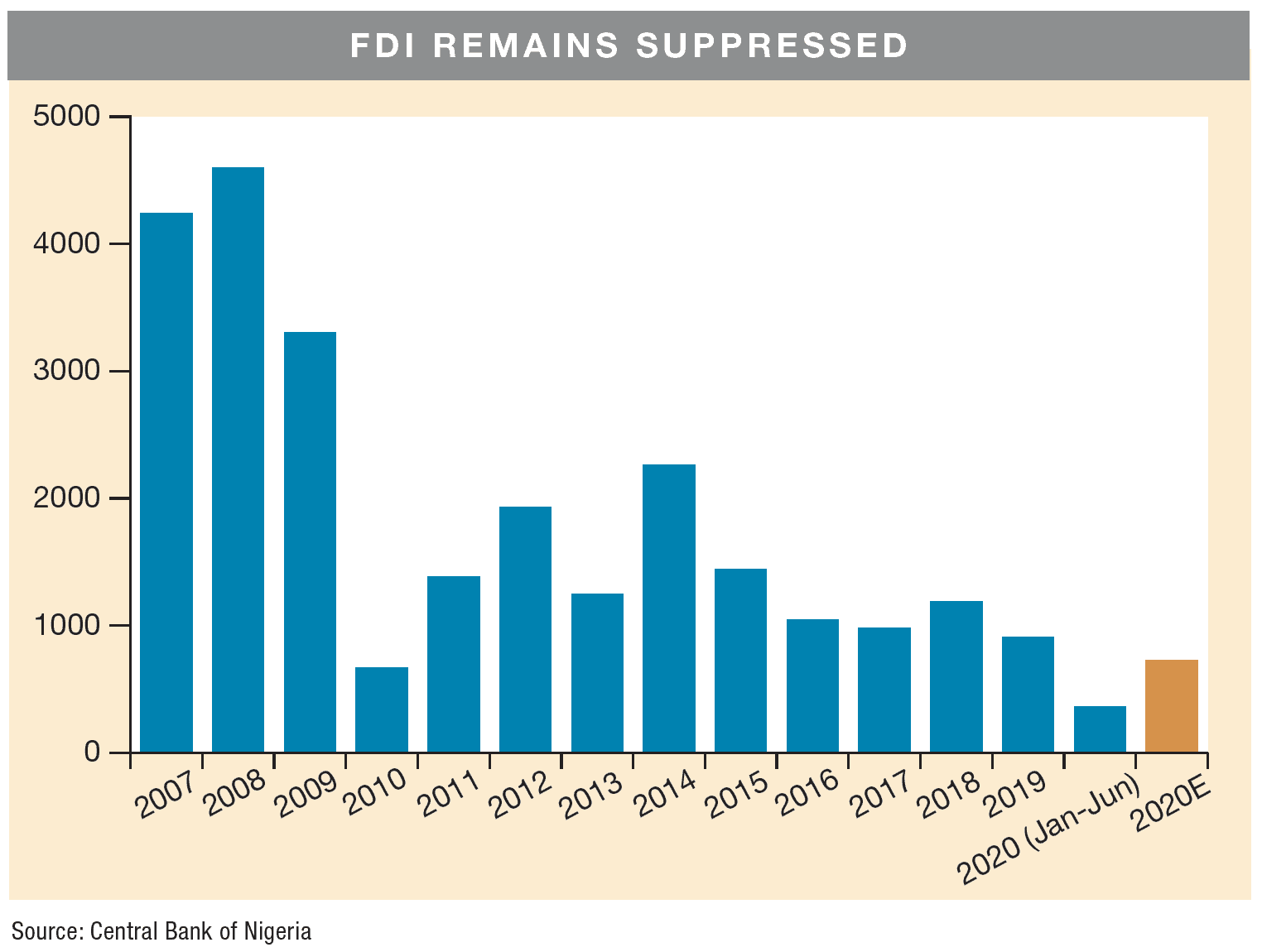

Despite numerous interventions and loan schemes by the government and the CBN, only a few businesses have received funding, Ogunkoya says. Businesses and individuals also must grapple with the absence of clear policies, erratic FX policies and high inflation—which also make it difficult for Nigeria to attract much-needed foreign direct investment.

“Nigeria made some progress at improving its investment environment; it’s jumped from 170 to 131 out of 190 countries in the World Bank’s “Ease of Doing Business ranking” during Buhari’s tenure. But there’s still plenty of work to be done,” says Patrick Curran, Senior Economist at Tellimer, notably dismantling a protectionist FX edifice the CBN erected.

Breaking Out of Recession

Most urgently, however, Nigeria needs a boost to aggregate demand to lift it out of recession, Adi says. Demand will go up when people have money in their pockets, raising their disposable income and purchasing power. That can’t be achieved when salaries are being cut and even basic items stay unsold.

Adi wants to see the government consider providing subsidies through conditional cash transfers to some people, which he contends will have a greater impact than cutting tax rates on personal or business income, since Nigeria already has a low tax-to-GDP ratio of 6.1% as of 2019.

In principle, Nigeria has room to inject some stimulus, Curran argues, since its debt stock is low relative to its peers; its public debt is expected to remain below 35% of GDP in 2020. But its revenue base is also among the lowest in the world, with consolidated revenue reaching less than 8% of GDP and federally retained revenue less than 3% of GDP in 2019—and likely to fall further in 2020 given falling oil revenues.

“As such, interest payments will consume nearly 100% of federal revenue this year, as per International Monetary Fund forecasts,” says Curran, “leaving little room for spending to stimulate the economy. Nigeria needs to broaden its revenue base if it hopes to implement expansionary fiscal policy, including through VAT hikes and a raft of administrative measures. Otherwise, low spending on physical and human capital will continue to be an impediment to growth.”

Nigeria’s deep capital markets can help to stimulate domestic consumption and break it out of the recession, but Curran fears this will crowd out private sector investment at a time when growth is already under pressure. Inflation is the other stumbling block. The difficulty of fashioning an effective stimulus package is compounded by the decline in the naira, which has eroded consumer purchasing power. Inflation rose to 13.7% in September, its highest level in two years, according to the National Bureau of Statistics. The government has set a year-end inflation target of 11.95 % for 2021.

Looming over these concerns are the country’s structural issues, says AZA’s Eduviere, and the chronic lack of political will to address them. “The biggest obstacle is politics,” he argues. “Diversification is the mantra during periods of crashing oil prices and recession, but these policies soon drift during the recovery phase. This is a cyclical phenomenon that Nigeria needs to break.”