Turmoil births innovation and the pandemic brought on both.

There was no olive oil before the Black Death. No pressurized airline cabins before World War II.

Turmoil births innovation. The notable fintech hubs, labs, incubators and accelerators examined by Global Finance this year have both turned to technology to function during Covid-19 and nurtured startups that help financial institutions operate in a socially distanced world.

“Due to Covid-19, face-to-face social relations have almost stopped,” says Soh Young, head of Seoul Fintech Lab. She’s not exaggerating. Social distancing helped South Korea limit cases of Covid-19 to about 80,000 and deaths to fewer than 1,500. “Various delivery services—in education, culture, finance and medical care—are expanding the range of things that can be done without interpersonal contact,” she adds. “The preference for noncontact types of finance is growing. Prior to the outbreak, it was clear that fintech would play a pivotal role in financial services. Covid-19 has undoubtedly accelerated that process.”

Young points to the emergence of robo-advisories, in which algorithms and artificial intelligence (AI) generate tailored investment strategies for customers, as one example. Two innovations to come from companies incubated in the Seoul Fintech Lab are a new platform providing digital, low-fee remittance to 46 countries, and mobile payment services for parking-lot operators.

Olivier Guillaumond, head of ING Labs, concurs. “Covid-19 really accelerated the whole digital transformation stream. It has also changed the behavior of users and clients. It has underpinned a faster evolution.” Guillaumond cites digital payments at ING: The number of those payments more than doubled to 560 million between 2019 and 2020—and 87% of those payments were made on mobile devices.

Guillaumond believes that the Covid-19 crisis merged with an existing movement toward digital transformation to create a “perfect storm” of fintech innovation. “Covid-19 exacerbated the need for digitization. Digitization creates more data. So now we have more data fueling AI, which leads to more personalized services,” he says. “It’s a positive circle.” That is to say, mostly positive; Guillaumond also notes that more data creates more breach vectors, adding that an increasing number of fintech startups focus on cybersecurity.

Innovation centers have many names—labs, incubators, hubs, accelerators—and they take many forms. Some offer soup-to-nuts programs serving up everything from mentoring, classes and coworking spaces to networking and access to finance. Others offer more narrowly defined, but still valuable, services. For example, Ecobank, based in Togo and operating in 33 African markets, recently debuted a sandbox that enables fintechs to access Ecobank’s application programing interface, for use in the fintech’s own solution development. The sandbox opened as part of Ecobank’s effort to accelerate partnerships with fintechs throughout the continent. It complements Ecobank’s annual Fintech Challenge. Running since 2017, the competition gives African fintechs the opportunity to pitch their solutions for potential partnerships with Ecobank.

In an era that demands nonstop fresh ideas and adaptability, building tools and structures to support new thinking is critical. The record crop of submissions in response to Global Finance’s third annual review of the world’s fintech labs illustrates the massive growth in interest. Our primary focus is labs that bring together externally unrelated entities—uniting startups with financiers and industry mentors, for example, or bringing finance-sector players together with government entities or nonprofits to support economic development. A substantial portion of this year’s entries described recently launched in-house labs, particularly at financial institutions. We have included these as separate category.

|

BANK-SPONSORED LABS |

|---|

Not surprisingly, the banking sector is a key locus of financial innovation, and bank-sponsored labs that support the fintech startup sector are among the strongest in this space.

Attijariwafa Bank Innovation Lab strives to imbue innovation into banking operations, while also expanding the fintech ecosystem in its home base of Morocco via outreach to startups and students. Its WeLab arm accelerates time-to-market for fintech products by gathering innovative ideas and human capital from across the bank, then developing proofs of concept for fintech products. Additional lab arms—including Smart Up & Ideation, WeDesign and WeCulture—forge strategic partnerships with outside institutions, including startups and universities, to design future-banking capabilities. Thus far, Wenov has worked with 120 startups, developing proofs of concept with 16. Funding for these startups is available via Wenov’s partnership with Morocco’s Center for Entrepreneurship and Executive Development incubator. Wenov also works with Al Akhawayn University in Ifrane to mentor undergrads studying fintech, with a particular emphasis on natural language processing, AI, data mining and blockchain.

Israel has long been a hub of tech innovation, which may be one reason Tel Aviv is where Citi Markets and Securities Services and Citi Treasury and Trade Solutions host Citi Innovation Labs. (Additional locations include Dublin, London, New York and Singapore.) To date, Citi’s labs have incubated more than 100 companies, which have together raised more than $1.5 billion from venture capital firms and investors. Startups focus on topics such as reporting and reconciliation, process automation, improving the client experience, AI, Machine Learning (ML), big data and forging corporate digital identities.

Citi Innovation Labs pivoted to a virtual format during Covid-19. Despite the challenges posed by the pandemic, the lab in 2020 facilitated more than 950 startup meetings and introductions across 35 markets. It collaborated with the Banque de France and other European financial institutions on the use of digital currency for interbank settlements. It entered a memorandum of understanding with the Inter-American Development Bank to collaborate on the acceleration of a blockchain ecosystem in Latin America and the Caribbean, and developed technology to digitize investor proxy voting systems.

Hosted by the International Bank of Azerbaijan, IBA Innovation Center cultivates a forward-thinking culture at the bank by helping internal teams develop out-of-the box solutions to banking challenges while concurrently working with startups to develop new products, services and solutions. Creating a fintech ecosystem in Azerbaijan is an additional goal.

Its work with startups includes hackathons, incubation for early-stage companies and acceleration for more mature businesses. Demo days provide vetted startups with the opportunity to pitch to members of a bank-sponsored investors club. Webinars cover everything from open banking, regtech and cybersecurity to AI and ML. In order to build a talent pipeline within Azerbaijan, IBA also hosts a technology academy to train students in advanced technologies and programming languages.

In Europe, OTP Lab by OTP Bank, launched in 2017, acts as the innovation hub of OTP Group. Its overall mission is to maximize the group’s innovation potential. The lab has five arms. Its flagship OTP Startup Partner Program is an international operation that gives scaleups and later-stage startups the chance to build relationships with OTP. This is a non-equity program, with no guaranteed funding. However, the lab typically pays for pilots, and contributes to the first six months of long-term collaborations between startups, scaleups and the OTP business units they serve. In addition, OTP Lab works in close collaboration with OTP Group’s venture capital arm, PortfoLion, which invests in innovative entities through six funds with €220 million ($267 million) in assets under management.

OTP Lab ran its third Startup Partner Program in the spring of 2020, despite the spread of Covid-19 in Europe. It accommodated 13 companies. Following a kickoff week in Budapest, the program pivoted to a fully online format, providing startups with 33 hours of remote workshops and 43 hours of online one-to-one mentoring. A virtual demo day gave startups significant international visibility, with more than 1,100 viewers tuning in. Four startups immediately continued their collaboration with their sponsoring OTP business units, and three others were expected to eventually partner with the bank. OTP forecasts that these new partnerships will generate a total value of €1.85 million by 2025. In the fall, the Startup Partner Program began its fourth session. For this session, the lab received 469 submissions from 51 countries. Fifteen startups were selected for pilots.

The mission of ING Labs isn’t to bring new products to market, says lab head Guillaumond, but to validate new businesses for ING and its clients. Businesses incubated focus on disruptive services for lending, trade, security, compliance, retail mortgages and improving consumers’ financial health. To develop and deploy these services, ING may either partner with an existing scaleup or form one of its own from among ING’s in-house talent pool.

The lab’s primary locations, in Brussels and London, scan the market for major scaleups that offer products ING believes can help it and its clients meet their financial goals. The lab then offers a one-year program to test scaleup products for commercial viability. During this year, scaleups receive access to master classes, ING’s technological infrastructure, business sponsorship and “anything ING has to offer,” Guillaumond says. Two other labs, in Amsterdam and Singapore, incubate earlier-stage startups.

Businesses scaled at ING Labs include Cobase. This company offers corporations a single point of access for all accounts and financial products, no matter how many banks and financial services providers they use. A second ING-scaled company, Katana, offers a trade discovery tool that employs machine learning to scan bond markets and detect anomalies, helping traders and portfolio managers find investment opportunities more quickly.

Raiffeisen Bank International’s Elevator Lab bills itself as the largest fintech and startup partnership in CEE—with tentacles in the fintech ecosystems of Albania, Belarus, Bosnia and Herzegovina, Bulgaria, Croatia, Kosovo, Romania, Russia, Serbia and Slovakia. The four-month Elevator Lab Partnership Program is for later-stage fintech startups. The program helps these startups improve their products and scale them internationally. While collaborating with RBI, selected startups work with bank mentors to develop proofs of concepts. Startups may receive funding through Elevator Ventures, RBI’s venture capital entity. Innovations in 2020 included products to digitize bank branch management, a customer experience management platform, and know your customer solutions.

Tatra Bank, an RBI subsidiary based in Bratislava, Slovakia, hosts its own Elevator Lab. It offers fintech startups the mentoring and education needed to scale their products and services. Startups work in conjunction with teams of bank market research experts, programmers, designers, data analysts and businesspeople. These teams strive to speed the development of the types of prototypes that can help the bank meet its digital goals. Previously focusing on the Slovakian market, the 2020 session of Elevator Lab took on a global reach, developing solutions to reenvision the bank for worldwide operations. To scale itself globally, the bank hopes to work with the lab to develop super apps (portals for a wide array of products and services), marketplaces for financial services, and a plug-and-play infrastructure for core banking services.

Recent innovations to come through Tatra Bank’s Elevator Lab include an application programming interface for businesses to improve payment reconciliations, and a game-like virtual reality application designed to teach financial literacy to Generation Z. The lab also hosts various business and technological lectures, events and hackathons.

Deutsche Bank’s five innovation labs are located in Europe, Asia and North America. They work with startups to identify, evaluate and enable the adoption of emerging technologies in support of Deutsche Bank’s overall digital strategy. Startups fostered have specialized in-network load balancing, improving the user experience, and machine learning, among other topics.

Bank-sponsored innovation labs also thrive in South America and Asia. In 2020, BTG Pactual’s boostLAB nurtured Mosaico Holding to and through a successful IPO on the Brazilian bourse. The lab works with startups and scaleups, in part through a six-month acceleration program with top-shelf industry mentors. The bank says 45 million people were impacted by the Lab’s output in 2020.

In Sao Paulo, inovabra lab sponsored by Banco Bradesco consists of internal entrepreneurship, international collaboration, a capital fund, an internal research team and a startup program forging strategic partnerships between the bank and fintech companies that offer products or services applicable to banking needs. In 2018, the bank launched the 22,000-square-meter inovabra habitat co-working space, housing more than 174 startups. A virtual version, founded in late 2020 to complement the in-person site, gathers companies from all over Brazil and, via a digital platform, enables those companies to access opportunities within Banco Bradesco and its partner companies. Thus far, more than 2,600 startups have registered to use the platform. They are analyzed by Banco Bradesco to see which ones offer products or services to meet specific business challenges.

DBS Asia X (DAX) is one of Singapore’s largest innovation centers. In its 16,000-square-foot co-working space, DBS employees, startups and the broader fintech community come together to innovate. Through its Startup Xchange, DAX has matched dozens of startups with operating units inside the bank, and with the bank’s SME clients.

Significant Startup Xchange innovations for 2020 include Face Your Future. This interactive digital experience leverages AI and facial recognition technologies to create a visualization of what the user will look like in old age. The program then estimates the cost of fulfilling the consumer’s retirement needs. Costs are calculated through a series of question about the user’s lifestyle and health-care needs. The bank expects Face Your Future will increase its volume of financial planning leads by 10% in Singapore and by 20% in certain other markets. A second innovation, the DBS Digital Exchange, is a fully integrated tokenization, trade and custody ecosystem built for investors to manage their digital assets.

Despite the challenges of 2020, DAX managed to host 39 physical events and 10 virtual events, including lectures on topics such as cybersecurity and the Internet of Things (IoT). In addition to fund innovation, DBS has instituted a new grant-access program. It finds suitable grants for DBS-eligible innovation projects. To date, the office has identified more than 200 grants and assessed more than 122 innovation projects for grant opportunities.

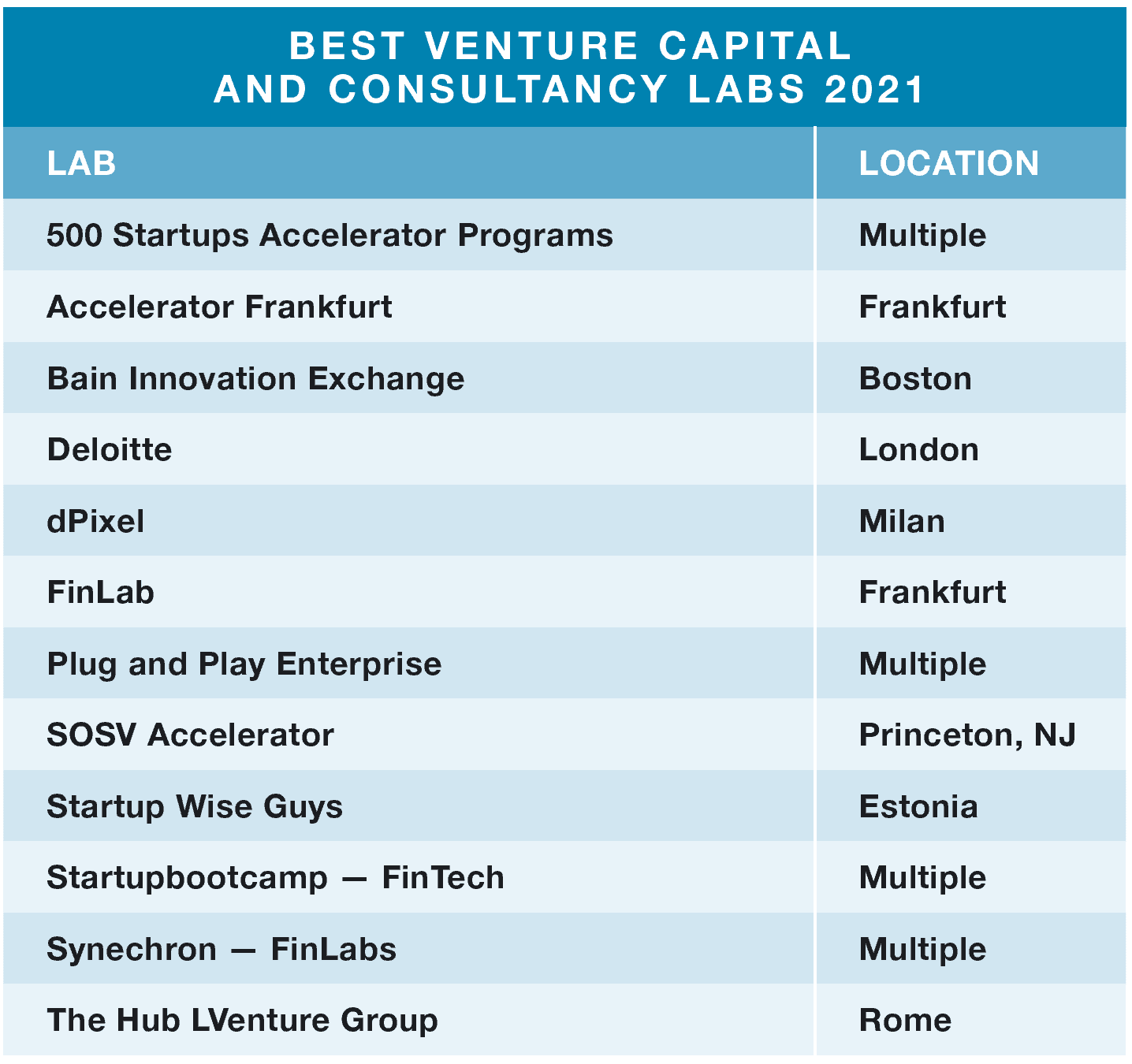

|

VENTURE CAPITAL AND CONSULTANCY LABS |

|---|

It’s no surprise to find venture capitalists supporting innovation labs–what better way to identify and build relationships with promising startups? Consultants, too, are finding value in the creative stimulation of hosting innovation labs.

Based in Sunnyvale, California, with 22 locations worldwide, Plug and Play bills itself as the world’s largest startup accelerator and Silicon Valley’s most active VC investor. It has accelerated more than 2,000 startups since 2006. Accelerated companies operate in eight different sectors, ranging from financial services to agriculture to retail. Its three-month fintech program runs twice a year and matches startups with the needs of financial institutions. Its goal is to launch pilots and proofs of concept while developing business opportunities. Increasingly, its startups are creating products designed to help businesses excel in a socially distanced world.

“Covid-19 has already changed financial services in so many different ways,” says Matt Helmers, Plug and Play’s director of strategy and business development. He points to wealth management and wealth transfer as an example. “If my parents die today, and I’m located in New York and they’re in California, how am I going to deal with wealth transfer?” he asks. “A lot of states require you to be present in the state” to make the transfer. He believes that post-pandemic, new wealth transfer procedures and technologies “will be a huge thing.”

Another VC firm accelerating startups is SOSV. Based in Princeton, New Jersey, its six-month program sees on-staff engineers, designers, scientists and mentors help accelerate startup development. The VC’s typical investment in the 150 companies it accelerates each year is $300,000. Lab innovations have focused on monetary decentralization and blockchain technology.

Accelerator Frankfurt is a VC and private equity firm offering a four-month, go-to-market program for B2B fintechs, along with startups operating in the fields of cybersecurity and insurance, among others. The accelerator offers startups mentorship, co-working spaces and professional services including strategy consulting, legal consulting and marketing. Seventy percent of startups accelerated find companies to fund their projects. New offerings in 2020 included acceleration programs focusing on women-owned businesses.

LUISS EnLabs is an accelerator run as part of The Hub LVenture Group lab. It is operated by the publicly listed LVenture Group in conjunction with Luiss Guido Carli University. At its 5,500-square-meter workspace hub, early-stage startups take part in a five-month immersive program. The lab provides companies with mentoring, management and opportunities for investor networking, as well as up to €200,000 per company in direct investment. Similar programs are run by FinLab in Frankfurt and 500 Startups in Mountain View, California (which charges a $37,500 fee to participate and typically offers an investment of $150,000 for a 6% stake in the startup). In Milan, dPixel runs a three-tiered program, consisting of preacceleration courses for startups at the idea stage, acceleration programs for startups with a clear business model, and matching programs connecting more established startups with corporations in search of innovation. Fintech areas of concentration include blockchain, AI and big data.

Consultancies host fintech labs to find solutions to client needs. Among the most significant are those hosted by Deloitte & Touche, Bain & Company and Synechron.

The internal Deloitte lab, called Catalyst, operates in the US and Israel. Catalyst consists of Deloitte innovation teams striving to create fintech solutions for the company’s institutional clients. Topics studied include IoT and digital transformation. Deloitte also hosts an external fintech accelerator in London, offering funding in exchange for a stake in the company.

At Bain Innovation Exchange, Bain professionals work with a network of established businesses, startups, venture funds and entrepreneurs to build, launch and scale disruptive new business products, market-test ideas, then pilot and scale new products. Based in New York, Synechron is an IT and consulting company with 13 fintech labs across the globe. Acceleration programs focus on AI, wealthtech and blockchain, among other topics. It has thus far accelerated more than 70 solutions in these fields.

|

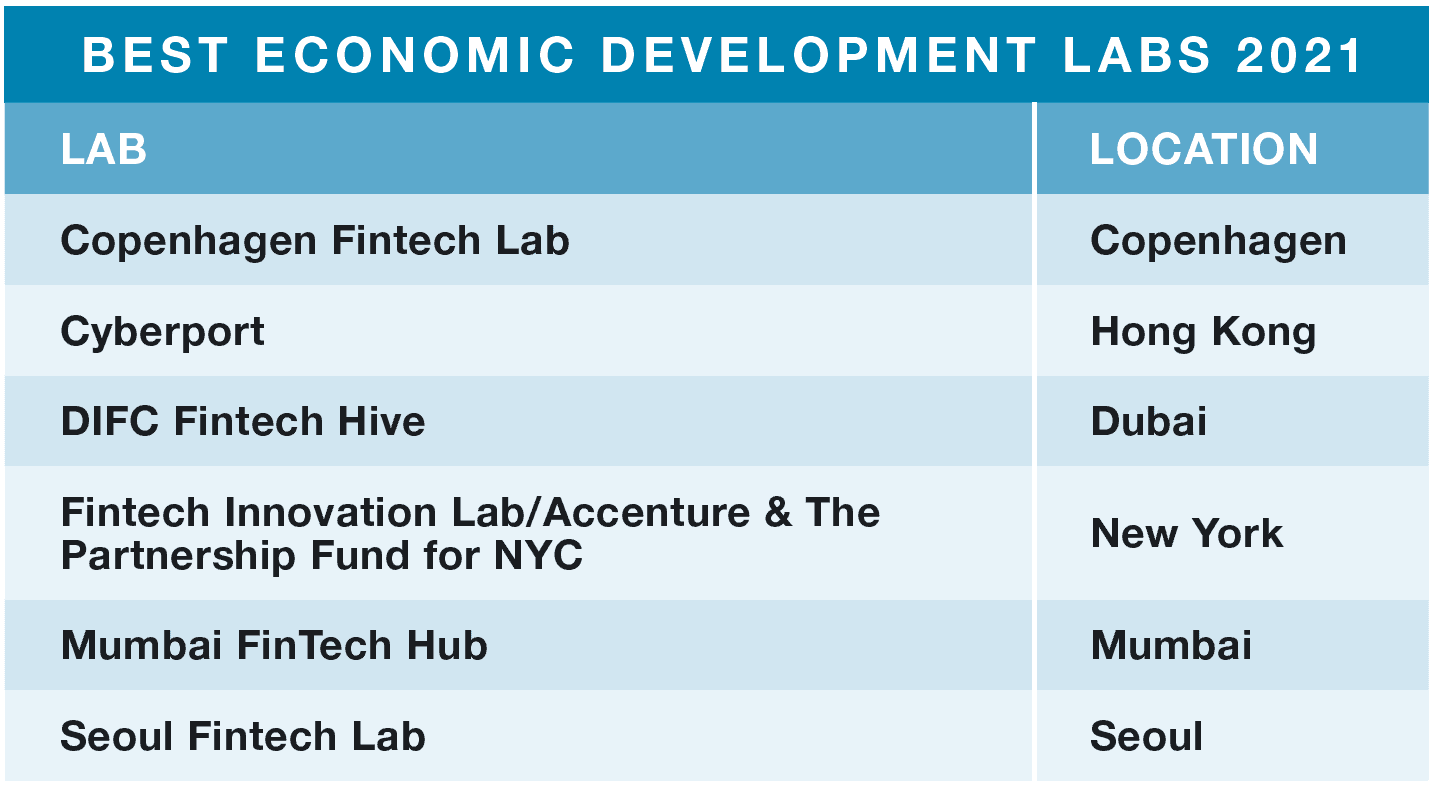

ECONOMIC DEVELOPMENT LABS |

|---|

Governmental organizations across the globe, finding that fintech innovation can bring value to entire communities, have launched their own innovation hubs.

The Seoul metropolitan government in 2018 launched Seoul Fintech Lab, which currently provides workspace for up to two years; a sandbox; monthly demo days; mentorship; investor relations days; marketing help; and classes in law, finance, taxation and labor relations. The lab also offers a two-track incubation/acceleration program: one for companies in operation three years or less, with fewer than five employees; a second for companies established less than seven years ago, with total sales above 100 million South Korean won ($88,000). No direct funding is offered, but startups can obtain up to KRW300 million through the lab’s relationship with the Korea Credit Guarantee Fund, and have access to members of the SFL ecosystem that may choose to invest. The lab has thus far incubated 96 companies that together obtained total investments of about $53 million.

In Dubai, DIFC Fintech Hive finds technological solutions for the challenges faced by finance companies in the Middle East, Africa and South Asia. Part of the Dubai International Financial Centre, this three-month accelerator operates in the fintech, insurtech and regtech fields. In 2020, it debuted a program to fund Series A+ startups and scale them throughout MENA. It also offered a new program for women-owned businesses.

The new tech internship program for youth at Cyberport, owned by the government of Hong Kong, is its latest effort to develop the fintech industry in that city. Cyberport startups focus on topics such as AI, big data and cybersecurity, with funding available to both start-ups and scaleups.

Mumbai FinTech Hub strives to generate next-gen fintech innovation in the Indian state, offering startups financial support, infrastructure, mentorship and funding. It is owned by the Government of Maharashtra and has engaged with more than 500 fintechs though more than 45 partner programs with tech companies, academic institutions and research labs.

The Copenhagen Fintech Lab provides programs aimed at everything from nurturing early stage fintechs to accelerating and scaling more established companies throughout the Nordics and the world.

Run by the Partnership Fund for New York City and Accenture, FinTech Innovation Lab is a 12-week program for early- to growth-stage startups. Since its inception in 2010, it has helped participants in its New York lab generate more than 280 proofs of concept and raise $1.4 billion in capital. Startups in its 2021 program focus on eliminating data silos, automating manual processes, connecting distribution platforms, implementing conversational analytics, AI and other topics. Its broad partner ecosystem includes Amex, Goldman Sachs and Chubb.

|

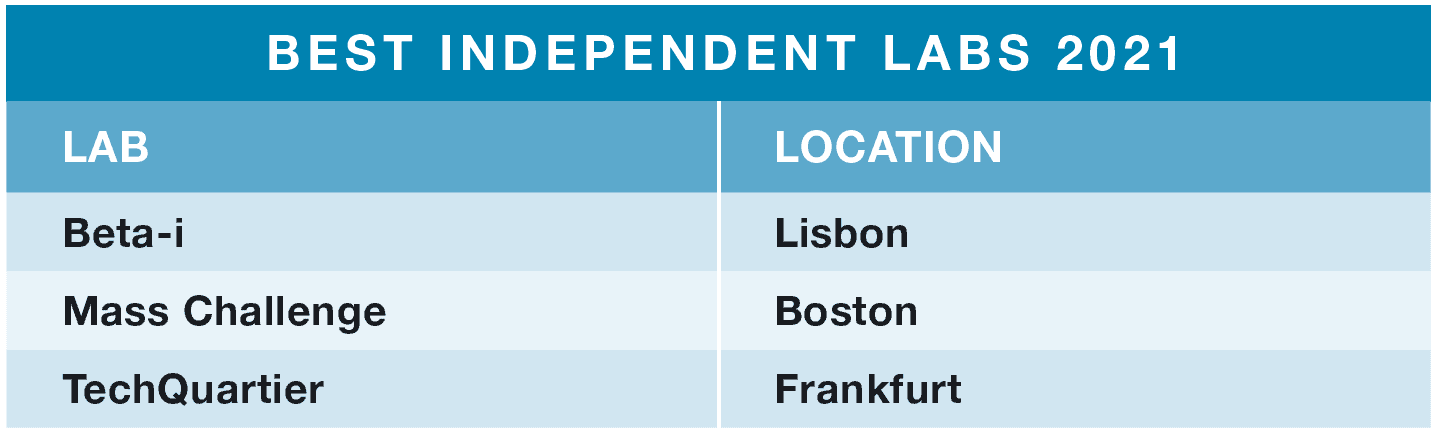

INDEPENDENT LABS |

|---|

These innovation centers are unaligned with banks, VC firms, or economic development organizations, and though they are few, their independence makes them stand out.

Mass Challenge is a 501(c) accelerator supporting early-stage startups. Its five-month program offers mentorship, training, office space, legal advice and access to funding. Among financial incentives are a $1 million annual prize doled out to a top startup. Mass Challenge takes no stake in the company in return for financial backing. It accelerates companies in nine different fields, including fintech. Its 2,400 alumni companies hail from 54 countries.

Based in Lisbon, Beta-i is an organization created to boost entrepreneurship. It helps new and established businesses grow by offering innovation services in the fields of acceleration, corporate innovation and education. It runs Lisbon Challenge, one of Europe’s most active startup accelerators. Beta-i also supports a fintech-only program called the SIBS Payforward Accelerator. (SIBS International is a payment-services company.) Over its 10-year history, Beta-i has incubated more than 1,500 startups from more than 80 countries, with more than 300 projects developed. Its broad partner ecosystem includes AWS, Microsoft, Novartis and BNP Paribas.

TechQuartier is based in Frankfurt and bills itself as “a creative arena and melting pot for entrepreneurs and innovators from the financial industry and beyond.” More than 40% of its 350 alumni startups work in fintech. TechQuartier’s broad partner ecosystem includes companies such as Visa, ING, IBM and Deutsche Bank.

|

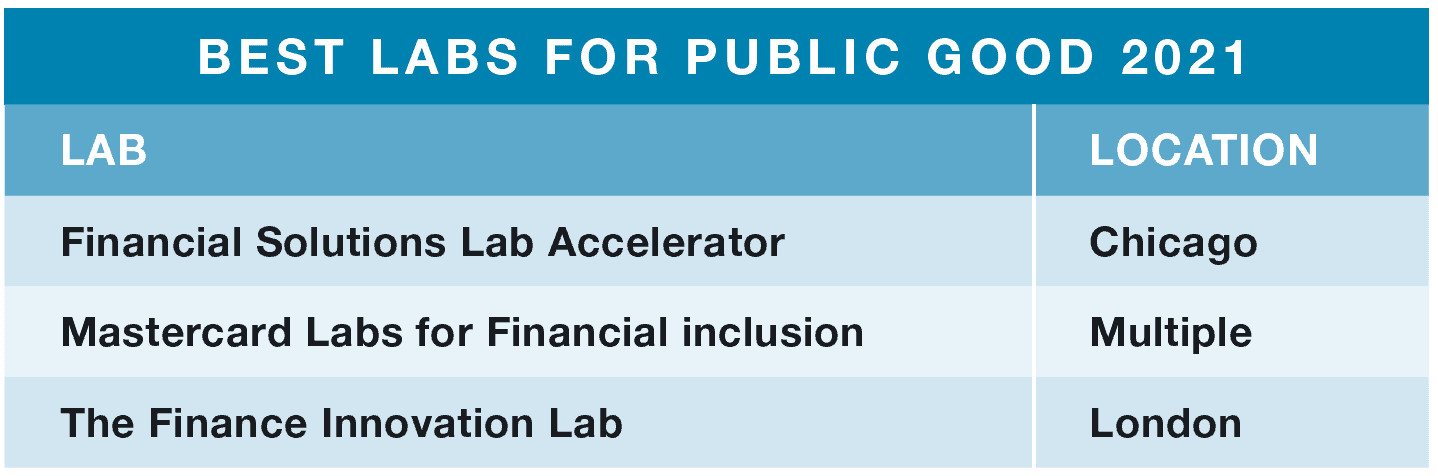

IN THE PUBLIC GOOD |

|---|

Some innovation labs seek to improve the financial lives of struggling people.

Headquartered in Nairobi and with nine innovation hubs from St. Louis to Singapore, the Mastercard Lab for Financial Inclusion seeks to create solutions for the two billion adults worldwide without access to mainstream financial services. Its $11 million grant from the Bill & Melinda Gates Foundation enables the lab to work with local entrepreneurs, governments and others to move fintech ideas from concept to reality. Its Kionect supply chain platform links microretailers, wholesalers and distributors of fast-moving consumer goods in underdeveloped countries. Kupaa is a platform implemented to digitize payments and information flows for schools Finally, the Mastercard Farmer Network digitizes marketplaces, payments and workflows between small farmers and the larger agricultural sector.

In Chicago, the Financial Solutions Lab seeks to “cultivate, support and scale innovative ideas that advance the financial health of low-to-moderate income individuals and historically underserved communities.” The lab is a $60 million initiative managed by the Financial Health Network and supported by JPMorgan Chase and Prudential Financial. Its accelerator works with startups to identify, develop and scale fintech solutions for targeted populations. It typically works with between four and eight companies a year, and each company accelerated receives a capital investment of $125,000, along with product development support, legal and regulatory guidance, and mentorship.

Its 2021 program, hosted virtually, focused on fintech solutions to help these populations improve long-term stability in the wake of Covid-19. Companies accelerated include Propel, a software company whose Fresh EBT program helps users manage their food stamp benefits, save money with coupons and explore job posts. A second alumnus, Digit, uses machine learning to analyze users’ income and spending to find small amounts of money they can save each day. Thus far, Digit customers have saved more than $2 billion.

A similar lab, geared toward “making data-driven finance work for people and the planet,” is offered by Future Finance’s The Finance Innovation Lab, based in London.

|

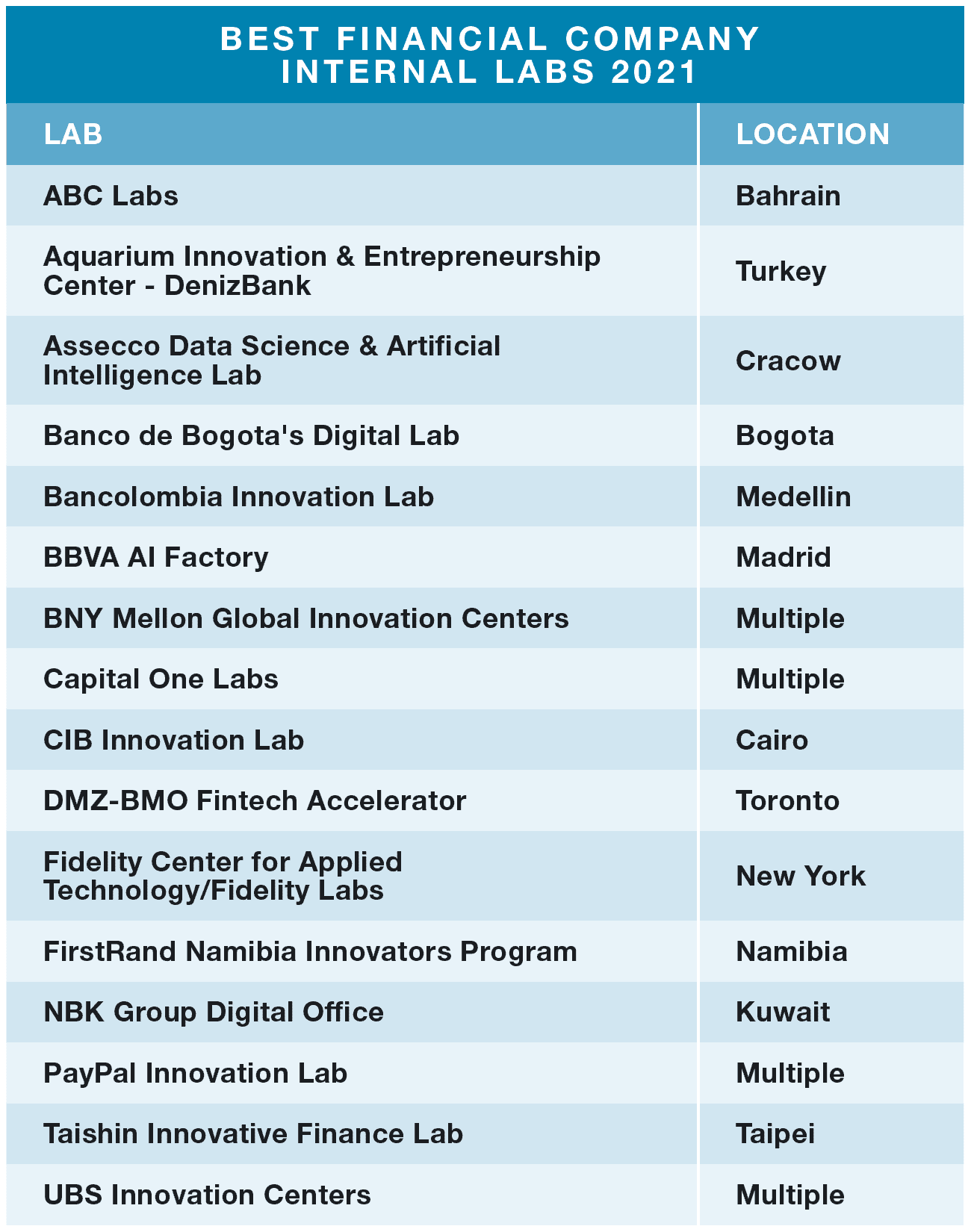

FINANCIAL COMPANY INTERNAL LABS |

|---|

With the capacity to innovate now seen as critical to survival, banks and other financial entities are increasingly creating their own in-house innovation “labs”—often a virtual team from different branches within the company—to focus on solutions for the future rather than the operations of today.

Internal innovation structures are spreading rapidly: Asseco Poland, for example, launched its internal lab in January last year. Many of the submissions in this category included information marked confidential, as these internal labs are focused on generating a competitive edge for the host bank. The internal lab at FirstRand Namibia saved the bank $3.5 million Namibian dollars ($25 million) just in 2020, as well as generating new income. UBS is leveraging cross-functional teams at offices in London, New York, Shanghai and Singapore to forge ahead with digital transformation in both services to clients and internally. During Covid, the teams were able to rapidly develop new products and capabilities for clients and for internal teams.

The internal innovation lab at Bancolombia strives to find fintech solutions to challenges faced by the bank and its customers. Significant developments from 2020 include a mobile platform for digital payments between consumers and store clerks, and between stores and their suppliers. The platform helps reduce inefficiencies associated with cash management throughout the distribution chain. Likewise, the BBVA AI Factory this past year devised five solutions that brought the bank improved margins or added capabilities that help build new products.

Banco de Bogota’s Digital Lab has one of the more established track records—founded in 2017—and has become, according to Digital Strategy Director Alejanddro Esguerra, “the main ‘placer’ of products within the Bank.” The Lab played a key role in developing several new products, including mortgage loans, digital payroll and payroll lending, insurance and investment.

Digital transformation is a top-of-mind driver for many financial services institutions, and internal labs often work to enable it. ABC Labs is the internal lab of the Kingdom of Bahrain’s Bank ABC. The bank wants to be MENA’s leading international bank. It strives to achieve digital leadership in the region—implementing mobile-only banking capabilities and deploying a state-of-the-art digital internal platform, among other initiatives. The lab supports bank transformation, researching and developing fintech solutions for Bank ABC and its subsidiaries, and improving products and services to drive adoption at scale. The lab is also organizing fintech forums in the Mideast and Africa.

In Cairo, the Commercial International Bank Innovation Lab focuses on internal innovation while also scouting startups for its Entrepreneurs Engagement Program. This program merges CIB resources with startup agility to source unique offerings that complement CIB activities. Innovations take place in the fields of e-commerce, digital payments, logistics, payroll, remittance and lending. Outreach includes hackathons and sponsorship of several fintech labs in the region. CIB professionals participate as judges, mentors and experts in a number of events.