Striving to shake its oil dependence, Kuwait is opening up to foreign ownership. Will investors bite?

When oil prices were more than $100 a barrel, Kuwait amassed substantial foreign exchange reserves, and those are helping the Gulf state weather the precipitous decline in crude prices.

With an output of about 2.8 million barrels a day, Kuwait is one of the biggest oil producers in the Gulf Cooperation Council (GCC), and its break-even price of around $48 a barrel (as estimated by the IMF) is the lowest in the group. Still, even with strong financial buffers, Kuwaiti leadership has signaled it intends to shake up the economy, maybe even tackling expensive subsidies. In January the government announced plans to develop five islands into special free-trade zones as the country ramps up plans for economic diversification—a model first championed by Dubai in the neighboring United Arab Emirates.

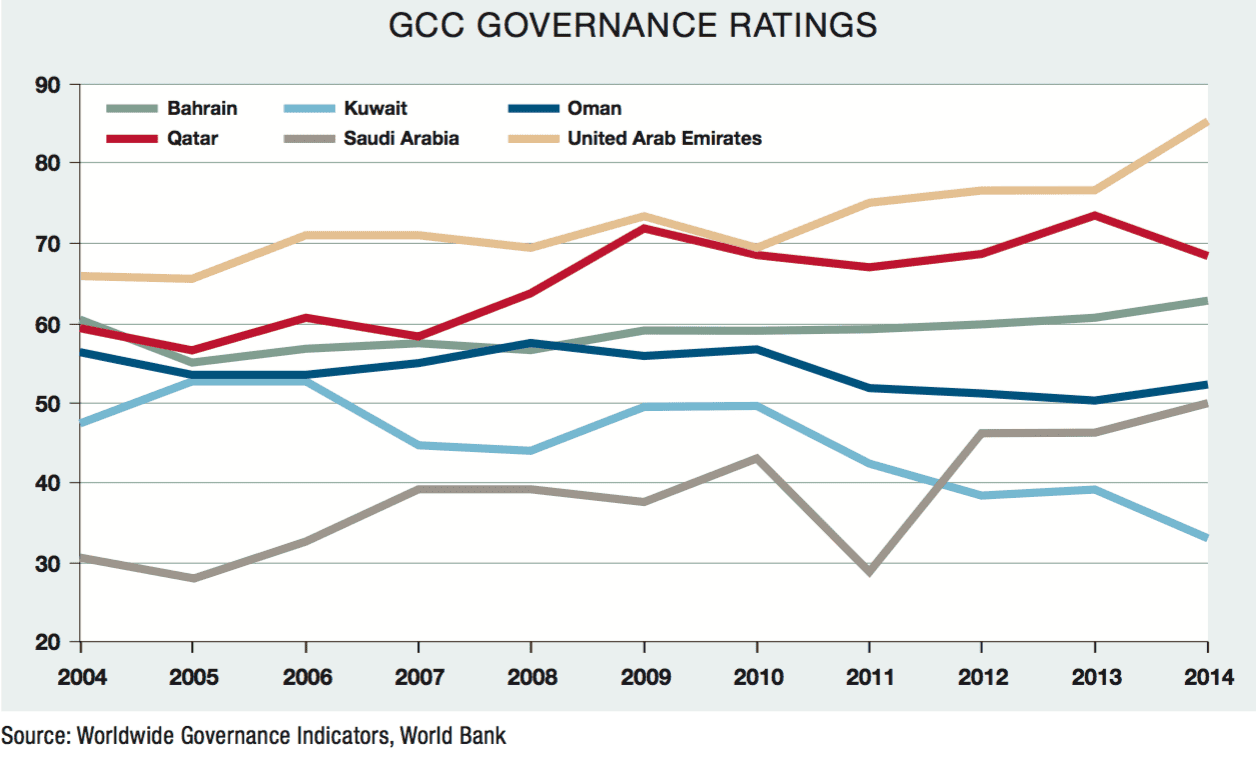

On the other hand, unlike Dubai, Kuwait has struggled to develop a significant non-oil sector and is still heavily reliant on hydrocarbon revenues, which have accounted for as much as 94% of government revenues, the highest among Gulf countries. Kuwait is also handicapped by a bureaucratic operating environment and standards of governance that lag the rest of the GCC, according to the World Bank’s Worldwide Governance Indicators (chart).

The credit rating agency Moody’s says Kuwait’s governance scores have been deteriorating because of long, burdensome executive and legislative processes. The often hostile relationship between the elected parliament and government has hampered economic reforms, leading some analysts to question the government’s ability to deliver on its diversification intent. It is a similar picture with the rule of law and control of corruption. On both of these governance measures, Kuwait scores below all other GCC states, according to the World Bank.

Boosting Private-Sector Participation

Kuwait’s weak institutional capacity worries investors, but there are signs political leaders aim to resolve their apprehension. The government has amended the public-private partnership (PPP) law to provide a transparent regulatory framework for a spate of planned infrastructure projects whose costs total 7.77 billion Kuwaiti dinars ($25.5 billion). The new rules permit full foreign ownership; so far, five projects have been approved without Kuwaiti partnership, says Dubai-based Arqaam Capital.

The emirate’s capital market laws have also been updated to encourage debt issuance and the transition of state-owned enterprises to public markets. Since the law’s amendment, $3 billion of securities in bonds and stocks have been issued, and $1 billion is in the pipeline to promote project development and increasing competitiveness. This will likely include privatization of ports, airports and some parts of Kuwait Petroleum and will be keenly watched by foreign investors. In its 20152016 Global Competitiveness Report, the World Economic Forum ranked Kuwait 34th out of 140 countries, up from 40th the previous year.

Analysts say that, after years of neglect, capital expenditure is essential—particularly in the power, water and healthcare sectors. These initiatives look timely, given Kuwait’s deteriorating fiscal position. Arqaam projects a budget deficit of 8.2 billion dinars and notes the government has approved a plan to impose a 10% corporate tax rate that domestic banks expect to be introduced in 2017—ahead of the rest of the GCC. The information and communications technology sector may garner new investment—upheaval in Syria could result in Kuwait’s becoming an international hub as an Internet protocol traffic line from Kuwait to Iraq and Iraq to Europe. Annual IP traffic growth in the Middle East is expected to reach 35%, says Arqaan.

Resilient Banking Sector

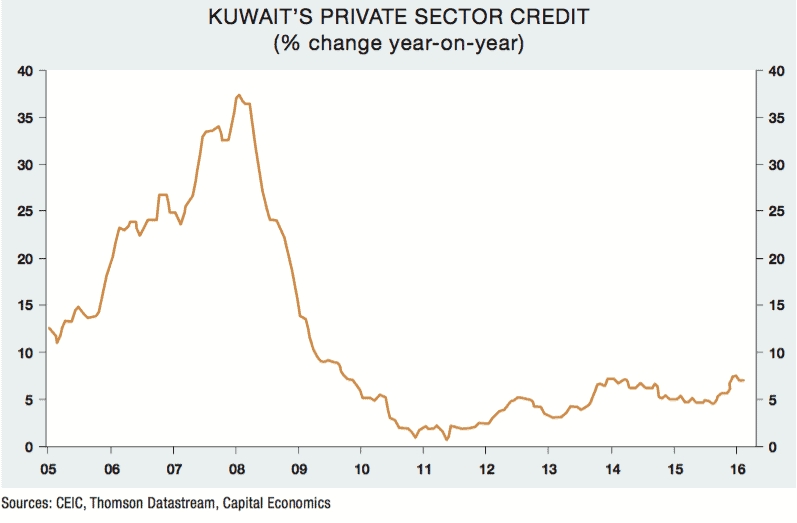

Although there is tightening regional liquidity, Kuwait’s banks appear better placed than most of its GCC neighbors to meet the challenge of lower oil prices. With around 5 billion dinars in liquidity, these banks have plenty of scope to fund potential projects and support government objectives. Permitting foreign investment in Kuwait is also likely to boost the domestic banking sector’s diverse lines of business, typically in advisory services, letters of credit and direct or syndicated financing. Private-sector credit growth nevertheless remains sluggish (chart); growth in credit card transactions has slowed.

Adding to the uncertain outlook, Kuwait’s decision to introduce a corporate tax and plans for a pan-GCC value-added tax bring to an end the region’s history as a tax-free location. Geopolitical risk and terrorist attacks could derail Kuwait’s bid for economic diversification and dampen banking profits. Still, the banking system is one of the Gulf’s strongest, and the prudent approach of the Central Bank of Kuwait (CBK) to provisioning suggests the banking system has substantial loss absorption capacity.

Moody’s believes Kuwait can withstand a severe stress scenario. High public-sector wages, a steady increase of Kuwaiti public-sector employees and hiring of skilled expats will continue to drive demand for consumer loans, although the pace of growth may moderate. The rate of project implementation is also improving, which is expected to boost new credit. Indeed, government spending will underpin a favorable operating environment for banks. The overhang of nonperforming loans—a legacy from the 20082009 financial crisis, which reached a peak of 10.2% in 2009—has fallen sharply, according to Moody’s. The agency forecasts the rate to ease to 3% this year. Even so, concentration risk and exposure to volatile equity and real estate markets pose challenges for the whole banking sector.

Capitalization also continues to improve. The CBK is conservatively introducing Basel III requirements on an accelerated schedule that will reach full implementation this year. According to the CBK, Kuwaiti banks should hold a minimum common equity Tier 1 ratio of 9.5%, total Tier 1 of 11% and total capital of 13% to risk-weighted assets. Kuwait’s implementation is 2.5 percentage points higher than the Basel committee’s recommendations.

Policy Dilemmas Continue To Weigh

Kuwait is not alone in being under pressure to diversify quickly. The region trails the global economy in productivity, and increasing inclusiveness remains a significant challenge. Improving female participation, expanding native-born employment prospects and reducing youth unemployment are key to the region’s short-term success, according to Oxford Economics, an independent advisory firm. It forecasts Kuwait’s economy to expand 2.3% this year. Despite large capital reserves, Kuwait’s huge dependence on hydrocarbon revenues means a further fall in oil prices could squeeze expenditure. And with a high public-sector wage bill, that may create political tensions.

Nevertheless, with indications that relations between parliament and government are warmer than they have been for some time, there is hope that major expenditure commitments will proceed unhampered. If so, Kuwait has the potential to be one of the Gulf’s few opportunities at a time of regional political uncertainty and economic austerity. That will be welcome news to investors seeking frontier market exposure.